Bidipta Sarkar∗1,2, Mattie Fellows∗1, Juan Agustin Duque∗2,3,

Alistair Letcher†1, Antonio León Villares†1, Anya Sims†1, Clarisse Wibault†1,

Dmitry Samsonov†6, Dylan Cope†1, Jarek Liesen†1, Kang Li†1, Lukas Seier†1, Theo Wolf†1,

Uljad Berdica†1, Valentin Mohl†1,

Alexander David Goldie1,2, Aaron Courville3,5, Karin Sevegnani4,

Shimon Whiteson‡2, Jakob Nicolaus Foerster‡1.

$^1$ FLAIR - University of Oxford, $^2$ WhiRL - University of Oxford, $^3$ MILA– Québec AI Institute

$^4$ NVIDIA AI Technology Center, $^5$ CIFAR AI Chair, $^6$ NormaCore.dev

{bidipta.sarkar, matthew.fellows, jakob.foerster}@eng.ox.ac.uk

juan.duque@mila.quebec, shimon.whiteson@cs.ox.ac.uk

Abstract

Evolution Strategies (ES) is a class of powerful black-box optimisation methods that are highly parallelisable and can handle non-differentiable and noisy objectives. However, naïve ES becomes prohibitively expensive at scale on GPUs due to the low arithmetic intensity of batched matrix multiplications with unstructured random perturbations. We introduce Evolution Guided GeneRal Optimisation via Low-rank Learning (EGGROLL), which improves arithmetic intensity by structuring individual perturbations as rank-rr matrices, resulting in a hundredfold increase in training speed for billion-parameter models at large population sizes, achieving up to 91% of the throughput of pure batch inference. We provide a rigorous theoretical analysis of Gaussian ES for high-dimensional parameter objectives, investigating conditions needed for ES updates to converge in high dimensions. Our results reveal a linearising effect, and proving consistency between EGGROLL and ES as parameter dimension increases. Our experiments show that EGGROLL: (1) enables the stable pretraining of nonlinear recurrent language models that operate purely in integer datatypes, (2) is competitive with GRPO for post-training LLMs on reasoning tasks, and (3) does not compromise performance compared to ES in tabula rasa RL settings, despite being faster. Our code is available at eshyperscale.github.io.

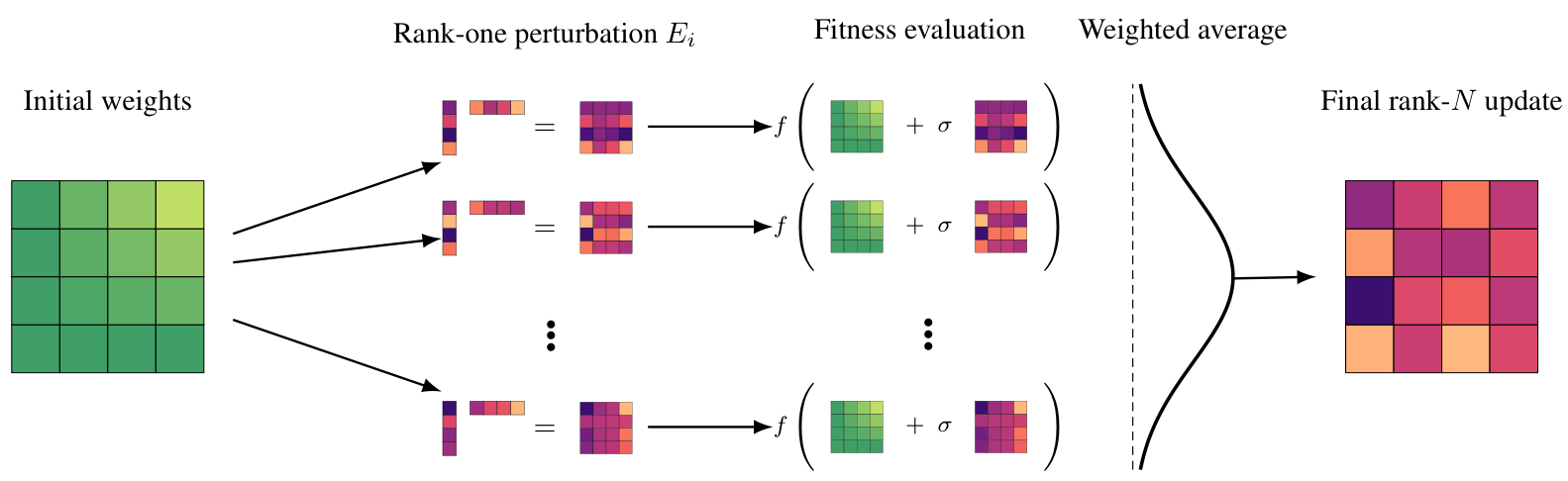

Figure 1: Schematic visualisation of EGGROLL using N workers.

1 Introduction

Evolution Strategies (ES) (Rechenberg, 1978; Beyer, 1995; Beyer & Schwefel, 2002)as established in prior literature is an attractive alternative to first-order methods based on gradient backpropagation for several reasons. First, ES does not require differentiability; it can optimise a broader class of models, like those with discrete parametrisations (cellular

*Equal Contribution † Core Contributor, sorted by alphabetical order in first names ‡Equal Senior Authors

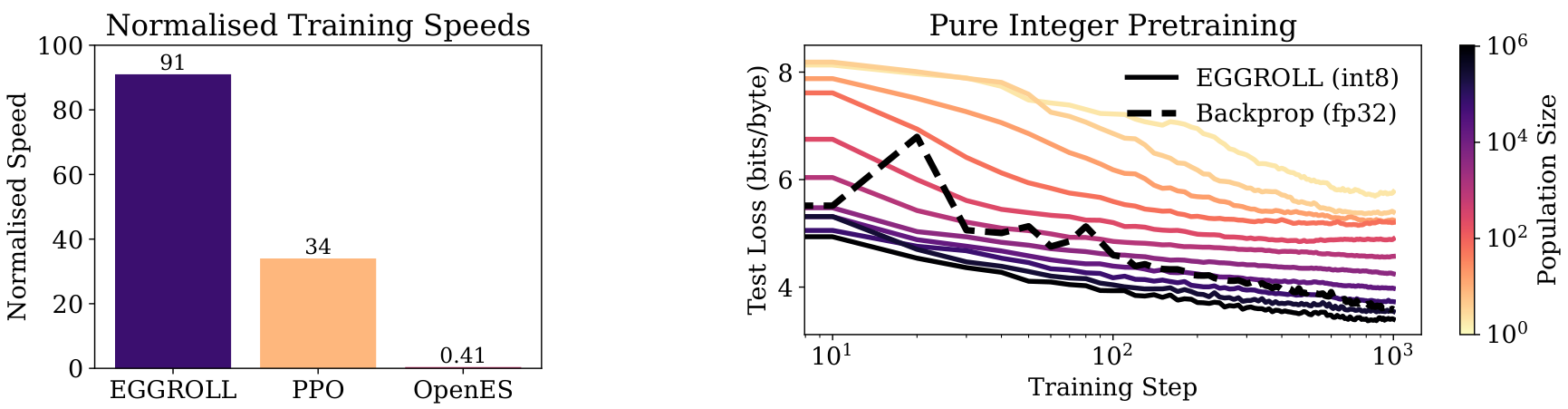

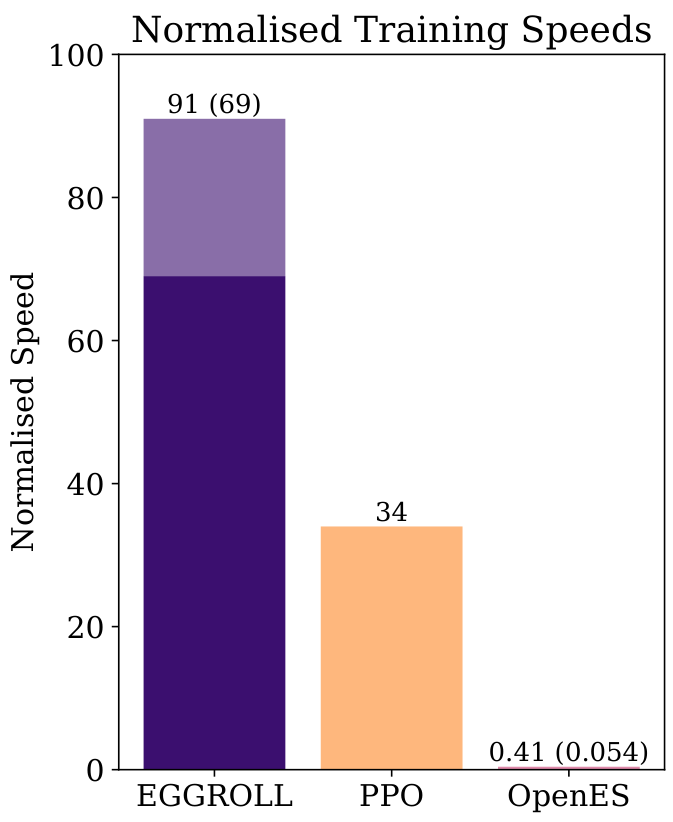

Figure 2: (a) Relative speed of our method, EGGROLL, in terms of experience throughput versus prior methods, where 100 is the maximum batch inference throughput. See Appendix E for more details. (b) We use EGGROLL to train an int8 RNN language model from scratch, scaling population size from 2 to 1,048,576 with a fixed data batch size of 16. The dotted line is a fp32 Transformer trained with backprop SGD. EGGROLL’s test next-token cross-entropy of 3.40 bits/byte while backprop only gets 3.58 bits/byte.

automata) or objectives for which gradients are unavailable or noisy, such as outcome-only rewards in LLM fine-tuning (Qiu et al., 2025). Second, ES can be more robust to noisy and ill-conditioned optimisation landscapes (Wierstra et al., 2011; Xue et al., 2021). Population-based exploration smooths irregularities (Salimans et al., 2017), tolerates discontinuities, and mitigates issues like ill-conditioned curvature or vanishing and exploding gradients in long-range or recurrent settings (Hansen, 2023). Third, ES is highly amenable to parallel scaling, since fitness evaluations are independent across population members and require only the communication of scalar fitnesses, which maps cleanly onto modern inference infrastructure and yields near-linear speedups on large clusters (Salimans et al., 2017). By contrast, backpropagation requires communicating and aggregating gradients across devices, yielding updates with high memory and computational costs. Furthermore, backpropagation requires special care when training models with low-precision datatypes (Fishman et al., 2025), whereas ES can directly optimise any model with the same datatypes used at inference time. Together, these properties position ES as a potentially powerful tool for training large, discrete, or hybrid architectures, and end-to-end systems with non-differentiable components, including LLMs (Brown et al., 2020; Chowdhery et al., 2023; Du et al., 2022; Fedus et al., 2022).

However, there are currently practical obstacles to employing ES at scale. In deep learning architectures (Goodfellow et al., 2016), the majority of trainable parameters form linear mappings represented by matrices (Rosenblatt, 1962; Hochreiter & Schmidhuber, 1996; Bengio et al., 2000; Krizhevsky et al., 2012; Goodfellow et al., 2014; Kingma & Welling, 2014; Vaswani et al., 2017). Naïvely adapting ES therefore requires generating full-rank matrix perturbations that replicate the entire parameter set for every population member. This inflates memory costs and forces frequent movement of large weight tensors. Evaluating these perturbations then requires a separate sequence of matrix multiplications per member, so the total compute and wall-clock time scale roughly with the population size and sequence length since batched matrix multiplication has a low arithmetic intensity, i.e., the ratio of arithmetic operations to memory traffic (Williams, 2008). In billion-parameter regimes, these two costs dominate, limiting ES to small models and small populations (Qiu et al., 2025; Korotyshova et al., 2025).

To mitigate both memory and computational bottlenecks, we introduce Evolution Guided GeneRal Optimisation via Low-rank Learning (EGGROLL), an ES algorithm that allows for the efficient training of neural network architectures with billions of parameters. Analogous to LoRA’s low-rank adapters in gradient-based training (Hu et al., 2022), EGGROLL generates low-rank parameter-space perturbations for ES; instead of sampling a full-rank matrix E∈Rm×nE in R m by n, we sample A∈Rm×rA in R m by r and B∈Rn×rB in R n by r with r≪min(m,n)r much less than the minimum of m and n and form E=r1AB⊤E equals one over the square root of r times A B transpose. This reduces auxiliary perturbation matrix storage from mn to (m+n)r per layer, and proportionally reduces tensor movement.

Moreover, we use a counter-based deterministic random number generator (RNG) (Salmon et al., 2011; Bradbury et al., 2018) to reconstruct noise on demand, so matrix perturbations need not persist in memory. When evaluating the fitness of members of multiple perturbations in parallel, EGGROLL batches a population of low-rank adapters and shares the base activations, enabling a single forward pass that applies all AB⊤A B transpose updates via specialised batched matrix multiplications with significantly higher arithmetic intensity, resulting

in over a hundredfold increase in training throughput for large neural networks at large population sizes, as shown in Figure 2a. Crucially, EGGROLL does not restrict updates to be low-rank, as the overall update is a weighted average of rank rr matrices across the population, making the matrix parameter update rank min(Nr,m,n)the minimum of N times r, m, and n.

To understand ES when applied to large parameter models, we analyse the convergence properties of general Gaussian ES in high dimensions, showing there exists a critical noise scaling σd=o(d−1/2)sigma d equals little o of d to the minus one half under which the update provably linearises and converges to the first-order derivative for a broad class of (possibly discontinuous) objectives. We identify three distinct regimes—linearisation, critical, and divergence—and establish provably tight conditions for stable ES optimisation in large models. Building on this, we extend the analysis to EGGROLL and prove that even fixed low-rank updates (including rank-1) converge to the true ES gradient as dimension grows, despite heavier-tailed perturbations. Our results explain the empirical success of EGGROLL in high-dimensional neural networks and connect its behaviour to neural tangent kernel-style linearisation (Jacot et al., 2018)Jacot and colleagues, yielding explicit convergence rates under standard overparameterised regimes. We also provide a rigorous theoretical analysis of the low-rank approximation accuracy, proving that EGGROLL updates converge to the full-rank Gaussian ES updates at a fast O(r−1)order r to the minus one rate.

Furthermore, in our extensive empirical evaluation, we test this hypothesis across a wide range of domains. In tabula rasa and multi-agent RL (MARL) settings, we show that EGGROLL does not compromise performance compared to naïve ES despite being faster. We demonstrate the scalability of EGGROLL for LLM fine-tuning with experiments on pretrained RWKV7 (Peng et al., 2025)Peng and colleagues models, modern recurrent language models that enable large batch inference due to their constant state size. Finally, we develop a nonlinear RNN language model that operates purely in integer datatypes, and demonstrate that EGGROLL can stably pretrain this language model, a feat which is only feasible due to the large population sizes enabled by EGGROLL.

2 Preliminaries

2.1 Low-Rank Matrix Approximations

When adapting high-dimensional foundation models for specific tasks, updating the parameters using gradient-based methods has high memory requirements. LoRA (Hu et al., 2022)Hu and colleagues applies low-rank approximations to the matrix multiplications to reduce these costs. For each matrix Mi∈Rm×nM i of dimension m by n in the model, a low-rank approximation can be made by decomposing each matrix:

Mi≈Mi0+AiBi⊤,

where Mi0:=StopGrad(Mi)M i zero is the imported matrix from the foundation model with frozen parameters and Ai∈Rm×rA i and Bi∈Rn×rB i are low-width column matrices (i.e., r≪min(m,n)r is much smaller than the minimum of m and n) whose parameters are updated through gradient-based optimisation during task-specific adaptation. This reduces the number of optimisation parameters for each matrix from mn to r(m+n). EGGROLL uses a similar low-rank approximation for evolutionary strategies.

2.2 Evolution Strategies

Evolution strategies (ES) (Rechenberg, 1978; Beyer, 1995; Beyer & Schwefel, 2002) is a set of black-box optimisation methods that has emerged as a useful alternative to first-order gradient-based methods like stochastic gradient descent (SGD), particularly for noisy or non-differentiable systems. Let f:Rd→Rf from R d to R denote an objective to be optimised, known as the fitness, where the goal is to find an optimising set of parameters x⋆∈argmaxx∈Rdf(x)x star. Each set of parameters is collected into a d-dimensional vector known as a genotype. We denote the derivative of the fitness ∇xf(x)∣x=a evaluated at x=a as ∇f(a). Unlike first-order gradient-based methods, which query derivatives ∇f(x) to update the vector of parameters x, evolutionary methods update a parametric population distribution over the fitness parameter space π(x∣θ)pi of x given theta, which is smoothly parametrised by a separate set of parameters θ∈Θtheta. The population distribution generates perturbations x∼π(x∣θ)x sampled from the distribution known as mutations. The problem of optimising the fitness f(x) for x reduces to optimising the parameters of the population distribution θ. This is achieved by solving a secondary optimisation problem to maximise the expected fitness under π(x∣θ) for θ:

J(θ)=Ex∼π(x∣θ)[f(x)].

Introducing a population distribution smooths the fitness landscape; since π(x∣θ)pi of x given theta is smooth in θtheta, the resulting objective J(θ)J of theta is also smooth in θtheta, provided f(x)f of x is measurable and integrable but not necessarily differentiable. Evolution strategies can therefore optimise black-box problems that may be non-differentiable as the derivatives of J(θ)J of theta exist for fitness functions that are discontinuous, yielding a gradient with respect to θtheta:

∇θJ(θ)=Ex∼π(x∣θ)[∇θlogπ(x∣θ)f(x)],

where ∇θlogπ(x∣θ) is known as the score function. A Monte Carlo estimate is formed by sampling N search mutations xi∼π(xi∣θ)x sub i sampled from pi and computing an average of the score-weighted fitnesses:

∇^θJ(θ)=N1i=1∑N∇θlogπ(xi∣θ)f(xi),(1)

with which we update θtheta via stochastic gradient ascent with a suitable stepsize αtalpha sub t:

θt+1←θt+αt∇^θJ(θt).

ES does not require taking derivatives directly through the fitness function; instead the Monte Carlo update in Eq. (1) only requires evaluation of f(xi)f of x sub i for each mutation xix sub i to estimate ∇θJ(θ)the gradient of J. As ES only queries f(x) and not ∇f(μ), it is a zeroth-order optimisation method.

In this paper, we study ES using Gaussian population distributions: π(x∣θ)=N(μ,Idσ2)pi of x given theta is a normal distribution with mean mu and covariance I d sigma squared. In addition to its mathematical convenience, the central limit theorem means that the Gaussian distribution emerges naturally from the EGGROLL low-rank approximation as rank increases, even if the matrices A and B are themselves non-Gaussian. Moreover, most widely-used ES algorithms assume Gaussian population distributions (Rechenberg, 1978; Schwefel, 1995; Hansen & Ostermeier, 2001a; Beyer & Schwefel, 2002; Auger & Hansen, 2011; Wierstra et al., 2011; Salimans et al., 2017). In our setting, ES optimises over the population mean μ∈Rdmu in d dimensional real space, which acts as a proxy for the true maximum of the fitness function, and the variance parameter σ2≥0sigma squared is treated as a hyperparameter to be tuned.

For the Gaussian population distribution we study in this paper, the ES update can be written using an expectation under a standard normal distribution by making a transformation of variables v=σx−μ(Wierstra et al., 2011; Salimans et al., 2017):

where v∼P(v)=N(0,Id) and p(v) denotes the density of P(v). In this form, Eq. (2) shows that Gaussian ES methods optimise the fitness by generating search vectors from a standard normal distribution N(0,Id) around the mean parameter μ.

2.3 Evolution Strategies for Matrix Parameters

A key focus of this paper is to develop efficient methods for evolution strategies that target matrix parameters. When working in matrix space, it is convenient to use the matrix Gaussian distribution (Dawid, 1981), which is defined directly over matrices X∈Rm×n:

where M∈Rm×n is the mean matrix, U∈Rm×m is the row covariance matrix and V∈Rn×n is the column covariance matrix. We use vec(⋅) to denote the vectorisation operator:

vec(X):=[x1,1,…xm,1,x1,2,…xm,n]⊤.

The matrix Gaussian distribution is a generalisation of the multivariate Gaussian distribution N(μ,Σ) defined over vector space. Sampling a matrix X∼N(M,U,V) from a matrix Gaussian distribution is equivalent

to sampling a vector vec(X)∼N(μ,Σ)vector X distributed as normal with mean mu and covariance sigma from a multivariate Gaussian distribution with mean μ=vec(M)mu equals vector M and covariance matrix Σ=V⊗Usigma equals V Kronecker product U where ⊗the symbol denotes the Kronecker product. For isotropic matrix Gaussian distributions with covariance matrices U=σImU equals sigma I m and V=σInV equals sigma I n, the equivalent multivariate Gaussian distribution is also isotropic with Σ=σ2Imnsigma equals sigma squared I m n. We denote the ℓ2L two vector norm as ∥⋅∥ and to measure distance between matrices, we use the Frobenius norm:

∥M∥F:=i,j∑mi,j2=∥vec(M)∥,

the Frobenius norm of M is defined as the square root of the sum of squared elements, which equals the L two norm of the vectorized matrix

which provides an upper bound on the matrix 2-norm (Petersen & Petersen, 2012). Let W∈Rm×nW in R m by n be a set of matrix parameters where vec(W)vector W forms a subset of the full parameter vector xx, typically parametrising the weights of a linear layer in a neural network. As we derive in Section B, the Gaussian ES update associated with the matrix WW is:

where MM is the mean matrix associated with WW, i.e. vec(M) forms a subset of μ, and P(E) is a zero-mean standard normal matrix distribution: p(E)=N(0,Im,In)p of E is a normal distribution with zero mean and identity covariance matrices. The gradient in Eq. (3) is estimated using the Monte Carlo estimate:

∇^MJ(θ)=σN1i=1∑NEi⋅f(W=M+σEi),

the estimated gradient is one over sigma N times the sum from i equals one to N of E i times f of W

by sampling NN search matrices Ei∼P(Ei) from a standard matrix normal distribution N(0,Im,In) around the mean parameter matrix M, which is updated via stochastic gradient ascent:

Mt+1←Mt+αt∇^MJ(θt).

3 Related Work

3.1 Evolutionary Algorithms

Evolutionary algorithms have long been a compelling alternative to backpropagation-based training methods (e.g., genetic algorithms (Such et al., 2018) or symbolic evolution (Koza, 1994)). Much research in evolution has focused on developing algorithms for deep learning that scale well to distributed parallel computation (Jaderberg et al., 2017; Hansen & Ostermeier, 2001b; Salimans et al., 2017). These approaches have increased in popularity following the application of ES to policy learning in deep RL environments (Salimans et al., 2017). Since then, evolution has been widely applied in other domains, such as meta-learning (e.g., (Lu et al., 2022; Metz et al., 2022; Lange et al., 2023; Goldie et al., 2024; 2025)), hyperparameter tuning (e.g., (Parker-Holder et al., 2021; Tani et al., 2021; Vincent & Jidesh, 2023)), and drug discovery (Towers et al., 2025). ES has also enabled the development of neural network architectures that are unsuitable for backpropagation, such as activation-free models that exploit floating point rounding error as an implicit nonlinearity (Foerster, 2017). Here, we consider how to apply ES at a scale beyond the small networks and population sizes of prior work. For example, Salimans et al. (2017)Salimans and colleagues use a maximum population size of 1440, whereas we use over a million.

While low-rank structures have been used in prior evolutionary algorithms, they have been applied to different ends, with different trade-offs, relative to EGGROLL. Choromanski et al. (2019)Choromanski and colleagues use a low-rank search space found via principal component analysis, which provides a better search direction to more efficiently use small populations. Garbus & Pollack (2025)Garbus and Pollack optimise a low-rank factorisation instead of the full dense matrix with neuroevolution, achieving similar computational gains to EGGROLL but is limited to the low-rank structure regardless of population size.

3.2 Evolution Strategies for LLMs

Although gradient backpropagation is typically used for LLM training and fine-tuning, prior work explores ES variants for fine-tuning. In particular, Zhang et al. (2024)’sZhang and colleagues’ two-point zeroth-order gradient estimator, which can be viewed as an ES-inspired method using a single perturbation direction and two function queries per update, is used by Malladi et al. (2023)Malladi and colleagues for memory-efficient LLM fine-tuning. Yu et al. (2025)Yu and colleagues extend this approach by projecting perturbations to a low-rank subspace, improving convergence. Jin et al. (2024)Jin and colleagues perform ES directly on LoRA matrices. These works focus on supervised fine-tuning and report performance comparable to full fine-tuning, but do not address whether pretraining is possible with two-point zeroth-order methods; we find that large population sizes are necessary for pretraining, indicating such methods are unsuitable here.

Recent work also explores ES in the context of LLM reasoning. Korotyshova et al. (2025)Korotyshova and colleagues first train LoRA adapters using supervised fine-tuning (SFT) before decomposing them into fixed SVD bases alongside singular values that are trained using CMA-ES. They achieve comparable performance to GRPO (Shao et al., 2024) in significantly less wall-clock time on maths reasoning benchmarks. Qiu et al. (2025)Qiu and colleagues directly use ES to optimise all LLM parameters for reasoning, with stronger performance than GRPO on the countdown reasoning task. However, both of these approaches use relatively small population sizes, on the order of a hundred unique perturbations per update, and instead collect hundreds of rollouts per perturbation to efficiently use GPUs. By contrast, our approach allows all generations to use different perturbations, such that our maximum population size per update is orders of magnitude larger (equal to the maximum inference batch size), without compromising token generation throughput.

4 EGGROLL

We now introduce EGGROLL (Algorithm 1). A practical issue with using a low-rank matrix approximation is that its distribution and score function have no analytic solution except for degenerate cases, so in Section 4.1 we derive the EGGROLL approximate score function from the limiting high-rank Gaussian. Section 4.2 describes how to efficiently implement EGGROLL on modern hardware.

4.1 Low-Rank Evolution Strategies

Recall the Gaussian matrix ES update from Eq. (3). Our goal is to introduce a tractable approximation to generating full-rank matrices by using low-rank matrices AB⊤A B transpose as our search matrices instead. Let p(A) and p(B) denote the distribution of A∈Rm×rA in R m by r and B∈Rn×rB in R n by r.

Assumption 1 (I.I.D. Sampling).Assume all elements ai,j∈A and bi,j∈B are continuous, identically and independently distributed random variables according to some zero-mean, symmetric, absolutely continuous distribution p0(⋅) with finite fourth-order moments and unit variance.

Algorithm 1 EGGROLL(r,α,σ,Tmax,Nworkers)

initialiseM and workers with known random seeds ς

forTmax timesteps do

for each worker i∈{1,…Nworkers}in parallel do

Ai∼p(Ai),Bi∼p(Bi)

Ei←r1AiBi⊤

fi←f(W=M+σEi)

end for

workers share scalar fitness fi with other workers

for each worker i∈{1,…Nworkers}in parallel do

reconstruct Ej for j∈{1,…Nworkers} from ς

M←M+αNWorkers1∑j=1NWorkersEjfj

end for

end for

This assumption is easily satisfied for most perturbation distributions used by ES, including members from the set of generalised Gaussian distributions like Laplace, normal, and uniform distributions. We then form a low-rank search matrix: E=r1AB⊤E equals one over the square root of r times A B transpose. The r1one over square root of r scaling ensures the variance of EE remains bounded for all rr. We denote the induced distribution of E as P(E). E=r1AB⊤ maps to the manifold Mr⊂Rm×n of rank-r matrices. Hence, the density p(E) is defined with respect to a unit volume on the manifold and cannot be defined with respect to the standard unit volume in Euclidean space. For the corresponding score function, gradients with respect to logp(E) are not defined over the usual Euclidean space. Instead, we use an approximation S^(E):Rm×n→Rm×n for the score function, yielding our low-rank update:

g^LR=−σ1EE∼p(E)[S^(E)⋅f(W=M+σE)].(4)

In our experiments, analysis and Algorithm 1, we use a Gaussian approximate score function:

S^(E)=−E,(5)

which is the score function for the Gaussian distribution N(0,Im,In)N zero, I sub m, I sub n. This choice is motivated by two theoretical insights from Section 5. The matrix AB⊤A B transpose can be decomposed as a sum of independent, zero-mean vector outer products. Under Assumption 1, the central limit theorem applies to this sum of variables, proving that P(E)P of E converges in distribution to a Gaussian N(0,Im,In)N zero, I sub m, I sub n as rank rr increases, recovering the approximate Gaussian score in the limit. Secondly, we investigate the convergence of ES and EGGROLL as the number of parameters grows, proving both updates converge to a linearised form that is consistent with the EGGROLL update using the Gaussian approximate score function.

EGGROLL is not wedded to any particular score function approximator and we derive and explore a set of mean-field approximators in Appendix D.1 as alternatives. However, our experiments show that the Gaussian approximator has the best overall performance on the tasks we consider. To optimise the ES objective using the EGGROLL update, we adapt the parallelised evolutionary strategies algorithm from Salimans et al. (2017)Salimans and colleagues. We make a Monte Carlo estimate of the expectation in Eq. (4) with NworkersN sub workers samples to optimise the mean matrix parameters MM using (approximate) stochastic gradient ascent. This yields the Gaussian EGGROLL update:

EGGROLL UPDATE: For each worker i (in parallel), sample Ai,t∼p(Ai,t), Bi,t∼p(Bi,t) and form a low-rank perturbation Ei,t=r1Ai,tBi,t⊤. Update matrix parameters using:

Here we absorb the constant σ1one over sigma into the tunable learning rate αtalpha sub t. As each random matrix Ei,tE sub i comma t in Eq. (6) has rank rr almost surely and the matrix is updated using a sum of NworkerN sub worker such matrices, the overall EGGROLL matrix parameter update has rank min(Nr,m,n)minimum of N r, m, and n almost surely, i.e., the overall parameter update is not restricted to be low-rank. For all experiments in Section 6, Nr>min(m,n)N r is greater than the minimum of m and n, i.e., EGGROLL parameter updates are full-rank.

4.2 Hardware-Efficient Implementation

A key reason to use EGGROLL over standard ES is that large populations can be simulated in parallel on a GPU thanks to the low-rank perturbations. For the sake of exposition, we write equations from the perspective of a single worker, ii, and explain in text how this corresponds to batched GPU operations. Consider the task of computing a batched forward pass over inputs ui∈Rdinu sub i in d in dimensional real space for a linear layer with mean parameter M∈Rdout×dinM of dimensions d out by d in. The standard forward pass is just a regular matrix multiplication, uiM⊤u i times M transpose, since MM is constant across all threads. In contrast, naïvely applying ES by trying to compute ui(M+σEi)⊤u i times the quantity M plus sigma E i transpose becomes a batched matrix multiplication, which is inefficient on GPUs since every element of M+σEi is only used in a single multiplication, yielding poor arithmetic intensity.

However, with EGGROLL we know that ui(M+σEi)⊤=uiM⊤+rσ(uiBi)Ai⊤u i M transpose plus sigma over root r times the quantity u i B i times A i transpose, which improves arithmetic intensity since it preserves the efficient general matrix multiplication used in batched inference while adding some additional cheap work per perturbation. In this context, the bulk of compute is spent on the efficient calculation of uiM⊤ using regular matrix multiplication. Meanwhile, when r=1r equals one, uiBiu i B i simply becomes an inexpensive batch of N vector-vector dot products of length din to get a batch of N scalars, which is then processed by a batched scalar-vector multiplication when multiplying by Ai⊤A i transpose. This decomposition is key to efficient batched LoRA inference, such as those used by vLLM (Kwon et al., 2023), which is why EGGROLL achieves the same speeds as batched LoRA inference systems. The batched LoRA inference enables high arithmetic intensity, enabling us to saturate compute with many unique perturbations per input. Note that this is impossible with naïve ES because each perturbation requires a separate matrix-vector multiplication, setting an upper bound of 1 for arithmetic intensity regardless of population size; see Appendix F for a full derivation.

We additionally optimise the update by not explicitly materialising the individual EiE sub i in the computation of ∑i=1NEifithe sum from i equals one to N of E i f i, the key term in the Gaussian approximate score function. In particular, when the rank is 1, we reconstruct A∈RN×dout and B∈RN×dinA of dimensions N by d out and B of dimensions N by d in and calculate the expression as (diag(f)A)⊤Bthe transpose of diagonal f times A, all times B, a simple matrix multiplication.

5 Analysis

*Proofs for all theorems can be found in Appendices A to D.*

In this section, we investigate the theoretical properties of the ES and EGGROLL updates. In Section 5.1, we study the convergence properties of the general Gaussian ES update as the parameter dimension d→∞d approaches infinity, obtaining the conditions required for convergence to a linearised form. We then extend this analysis to the EGGROLL update in Section 5.2. Finally, in Section 5.3 we provide an analysis investigating the effect that increasing the rank of the EGGROLL approximation, proving convergence to the true ES update in the limit.

5.1 High-Dimensional Gaussian ES

We first analyse the general ES update under Gaussian perturbations from Eq. (2):

∇μJ(θ)=σd1Ev∼N(0,Id)[v⋅f(μ+σdv)],

The gradient of J with respect to mu equals one over sigma d, times the expected value over v drawn from a standard normal distribution, of v times f of mu plus sigma d v

where v∈Rdv is a d dimensional vector. In high dimensions, the Gaussian annulus theorem (Vershynin, 2018; Wegner, 2024) proves that the probability mass of standard Gaussian distributions concentrates in thin shells of radius dthe square root of d, which place probability mass further from the origin as dimension dd increases. To counter this, we let σdsigma d depend on dd and analyse the critical decay rate of σdsigma d that yields convergence of the ES updates. We make the following mild regularity assumptions:

Assumption 2 (Locally Continuous Fitness).With probability 1 with respect to the random initialisation of μmu, assume there exists a ball Bρ(μ):={x′∣∥x′−μ∥<ρ}B rho of mu, defined as the set of x prime such that the norm of x prime minus mu is less than rho of fixed radius ρ>0rho greater than zero where f(x) is C1-continuous for all x∈Bρ(μ). Within this ball, let ∇f(x) be α-Hölder continuous, i.e., ∥∇f(x)−∇f(y)∥≤L∥x−y∥α for all x,y∈Bρ(μ), α∈(0,1] and L=O(1).the norm of the gradient of f at x minus the gradient of f at y is less than or equal to L times the norm of x minus y to the power of alpha, where alpha is between zero and one and L is of order one.

Assumption 2 does not restrict the fitness to be globally continuous; with probability one with respect to the initialisation distribution there must exist an arbitrarily small C1-continuous ball around μmu. In particular, discontinuities, kinks, and non-differentiable regions may exist in the domain, provided they are not encountered with nonzero probability in the local region explored by the algorithm. α-Hölder is the weakest simple, dimension-robust assumption that guarantees vanishing local gradient variation under Gaussian perturbations; it is weaker than Lipschitz continuity, which is recovered with α=1.

Assumption 3 (Global Polynomial Growth).Assume that there exists some constant 0<C<∞ that is O(1) in d and finite polynomial degree p≥0 such that ∣f(μ+σdv)∣≤C(1+∥μ+σdv∥p) and ∥∇f(μ+σdv)∥≤C(1+∥μ+σdv∥p) almost surely under v∼N(0,Id).Assume that there exists some constant C and finite polynomial degree p such that both the function f and its gradient are bounded by C times one plus the norm of mu plus sigma d v to the p-th power, almost surely under the normal distribution.

Unlike Assumption 2, this is a global assumption. Again, discontinuities can exist. The assumption is weaker than boundedness, is satisfied by essentially all fitness functions used in ES, and ensures that both the objective and its gradient are integrable under Gaussian perturbations; objectives violating this condition typically exhibit super-polynomial growth and derivative growth, which leads to ill-defined or highly unstable ES updates. Moreover, if the condition is not satisfied almost surely, then the function and its gradients are undefined in regions that have nonzero Gaussian measure.

Assumption 4 (Bounded Derivative).With probability 1 with respect to the random initialisation of μmu, assume that ∥μ∥=O(1) and ∥∇f(μ)∥=O(1), i.e. ∥μ∥ and ∥∇f(μ)∥ do not grow with increasing d.

This assumption is standard in high-dimensional analysis proving convergence to linearity, as proving convergence to ∇f(μ)the gradient of f at mu becomes meaningless if ∥∇f(μ)∥→∞the norm of the gradient approaches infinity. Moreover, the ES update as a whole can diverge if Assumption 4 is not satisfied. It can be ensured by scaling, typically by scaling networks parameters by d−1/2d to the minus one half or using an appropriate scaled initialisation, commonly Gaussian initialisation μ∼N(0,d1Id)mu distributed as normal with mean zero and covariance one over d times the identity matrix. This is precisely the scaling employed in the neural tangent kernel (NTK) regime (Jacot et al., 2018; Lee et al., 2019; Chizat et al., 2019), where it guarantees dimension-independent gradients and stable training dynamics.

These assumptions encompass essentially all objectives encountered in modern machine learning, including networks with finitely many ReLU activations, max- and hinge-based losses, and other piecewise-smooth or discontinuous models. Our first theorem proves convergence of a Gaussian ES update to a linearised form, that is to the local first-order derivative ∇f(μ)the gradient of f at mu, with a tight convergence rate for any function satisfying these assumptions:

Theorem 1 (Convergence to Linearity). Let Assumptions 2, 3, and 4 hold and σd=o(d−21)sigma d is little o of d to the minus one half. Then:

∥∇μJ(θ)−∇f(μ)∥=Θ((σdd)α)=o(1), almost surely with respect to the distribution over μ.

To understand the effect that breaching the σd=o(d−21) rate has on the convergence of Gaussian ES, we study the space of functions that can be represented by cubic polynomials of the form:

f(x)=a⊤x+21x⊤Bx+61C(x,x,x),(7)

where a∈Rd,B∈Rd×da in R d and B in R d by d is a symmetric matrix and C(x,x,x)=∑i,j,kci,j,kxixjxk denotes a symmetric 3-linear map represented by the symmetric 3-tensor C∈Rd×d×dC in R d by d by d, which generalises cubic equations of the form f(x)=ax+bx2+cx3 to vector-valued x. These are non-pathological, well-behaved, analytic C∞-continuous functions, and include a rich subclass of convex optimisation problems, for instance, cubic perturbations of strictly convex quadratics. Moreover, any convex C3-continuous objective admits a local third-order Taylor expansion of this form around a minimiser.

Theorem 2 (Exact Divergence for Cubic Objectives). Let f(x) denote the cubic polynomial in Eq. (7). Assume ∥a∥=O(1),∥B∥=O(1),∥C∥=O(1) where ∥⋅∥ denotes operator norm for i-tensor T(x1,…,xi): ∥T∥:=sup∥x1∥=⋯=∥xi∥=1∣T(x1,…,xi)∣. Let Assumption 4 hold, then:

Together, Theorems 1 and 2 prove Gaussian ES has a critical convergence rate of σd=o(d−21) in high dimensions, and operates in three regimes:

Regime I (Convergence to Linearity): For σd=o(d−21), ES converges to a linearised form, recovering a local first-order gradient update ∇f(μ). This result is analogous to neural tangent kernel (NTK) type theorems, which prove that neural networks linearise in high dimensions (Jacot et al., 2018)Jacot and colleagues, 2018 and results from the concentration of the population distribution as d→∞, but applies to a more general set of objectives including discontinuous architectures. Moreover, Theorem 1 proves that the (σdd)α rate at which Gaussian ES converges is tight and cannot in general be improved upon without strengthening continuity or introducing specific structure into the objective to ensure the Hölder constant L decays with d; for the class of cubic functions we consider in Theorem 2, the faster σd2d convergence rate found in Eq. (9) is possible due to the C∞-continuity of this function class, which means the converge rate is governed by third order derivative terms.

Regime II (Critical): For σd≍d−21, Gaussian ES converges to a nonlinear limiting update that may retain higher-order derivative terms when they exist; for our cubic example, Eq. (8) proves that at this critical rate, the second-order term associated with the matrix B vanishes due to symmetry and the third-order term associated with the tensor C remains:

2σd2Ev∼N(0,Id)[C(v,v,⋅)]=Θ(1).

As the polynomial form is representative of general Taylor expansions, this implies that the limiting high dimensional update retains third-order derivatives (and higher order odd derivatives) as d→∞.

Regime III (Divergence): For d−21=o(σd)d to the minus one half being little o of sigma d, Theorem 2 shows that there exist smooth cubic objectives with bounded coefficients for which:

∥∇μJ(θ)∥=Θ(σd2d)→∞.

the norm of the gradient of J with respect to mu is of the order sigma d squared times d, which goes to infinity

In particular, divergence occurs whenever the cubic tensor has a non-vanishing Gaussian contraction (equivalently, non-zero partial trace), i.e. in non-degenerate cases; only in the exceptional trace-free case does the cubic contribution vanish.

In practice, σdsigma d is often absorbed into the ES update stepsize, and its scale is adjusted automatically as part of the hyperparameter regime to ensure stability.

5.2 High-Dimensional EGGROLL

We now extend our high-dimensional analysis to study the EGGROLL update using the Gaussian approximate score function g^LRg hat L R from Eq. (5). Taking rr as fixed, we consider the Gaussian matrix ES setting outlined in Section 2.3. We take x=Vec(W)x equals Vec of W where W∈Rm×nW is an m by n matrix and analyse the effect of increasing the total number of matrix parameters d=mnd equals m times n. Recall the true ES Gaussian matrix update is:

∇MJ(θ)=σ1EE∼P(E)[E⋅f(W=M+σE)],

the gradient of J with respect to M is one over sigma times the expectation over E of E times f of M plus sigma E

where M is the set of mean matrix parameters associated with the matrix W and P(E) is a zero-mean standard normal p(E)=N(0,Im,In)p of E is a normal distribution with zero mean and identity covariance matrices.

Two key differences between full-rank Gaussian ES and EGGROLL are that g^LRg hat L R is an approximation to a true gradient and P(E) may have heavier tails than a Gaussian. To account for these differences, we require a slightly stricter local continuity control assumption:

Assumption 5 (EGGROLL Locally Continuous Fitness). With probability 1 with respect to the random initialisation of μmu, assume there exists a ball Bρ(μ):={x′∣∥x′−μ∥<ρ}B rho of mu, defined as the set of points x prime such that the distance to mu is less than rho of fixed radius ρ>0rho greater than zero where f(x) is C2-continuous for all x∈Bρ(μ) and ∥∇2f(μ)∥ be polynomial bounded in d. Within this ball, let ∇2f(x) be Lipschitz continuous, i.e. ∥∇2f(x)−∇2f(y)∥≤Ld∥x−y∥ for all x,y∈Bρ(μ).

This assumption still permits discontinuous objectives. We also assume that p0(⋅) generates sub-Gaussian elements with uniform tail control:

Assumption 6 (Sub-Gaussian Tails). In addition to Assumption 1, assume that p0(⋅) generates variables that have sub-Gaussian tails, i.e. for xi∼p0(xi):

P(∣xi∣>t)≤2exp(−Ct2),

the probability that the absolute value of x i is greater than t is less than or equal to two e to the minus C t squared

for some 0≤C<∞ that does not depend on d.

We discuss sub-Gaussian variables and their properties in Section C.3 The assumption is trivially satisfied for Gaussian distributions a∼N(0,Im) and b∼N(0,In), and holds more generally, for example for bounded distributions, uniform distributions and generalised Gaussian distributions with shape parameter greater than two. This flexibility is particularly relevant for the models in Section 6.1, where heavier-shouldered distributions may be preferred over the Gaussian.

Theorem 3 (EGGROLL Convergence to Linearity). Let W∈Rm×n, d=mn and x=Vec(W). Let Assumptions 3, 4, 5 and 6 hold, σd=o(d−1/2), and Ld(σdd)2=o(1). Then there exists some K>0 such that:

almost surely with respect to the distribution over μ.

Our theory explains the success of EGGROLL in high dimensions with rank as small as r=1r equals one; Eq. (11) proves EGGROLL converges to the true update matrix ES update ∇MJ(θ)grad M J of theta as d→∞d goes to infinity regardless of rr. In addition, Eq. (10) proves that under the same conditions, the EGGROLL update also linearises like the true Gaussian ES update analysed in Section 5.1, recovering a local first-order derivative as d→∞d goes to infinity. For high-dimensional neural networks, standard parametrisations place training in the NTK regime, in which the network behaves approximately linearly in its parameters and gradient descent converges to a global minimum (Jacot et al., 2018; Lee et al., 2019; Chizat et al., 2019)as shown in prior research. Recent results show that the spectral norm of the Hessian decays polynomially with width, and that higher-order derivatives governing the variation of the Hessian also vanish (Liu et al., 2020). Consequently, the Lipschitz constant Ld=o(1)L d is small o of one, typically at rate d−21 or d−1 depending on the network architecture. Substituting these rates into our upper bound in Eq. (10) yields convergence rates of O(σd2d23) or O(σd2d) respectively.

5.3 Rank Analysis

We now analyse how fast the low-rank update from Eq. (4) with Gaussian score approximation converges to the true Gaussian ES matrix gradient in Eq. (3) as the rank of the update rr increases. We make notation explicit in rr in this subsection, for example writing Er=r1ArBr⊤E r equals one over the square root of r, times A r B r transpose. We introduce the following formal regularity assumption for the fitness function:

Assumption 7 (Bounded Fitness). Assume that f(W)f of W is bounded, that is supW∣f(W)∣<∞the supremum over W of the absolute value of f of W is finite.

Our key theoretical result characterises the error rate between the Gaussian score approximator in the low-rank update g^LRr from Eq. (4) and the true gradient using the matrix Frobenius norm:

Theorem 4 (EGGROLL Rank Convergence). Let Assumptions 1 and 7 hold, then:

∥g^LRr−∇μJ(θ)∥F=O(r−1).(12)

the Frobenius norm of the difference between the low rank estimate and the true gradient is of order r to the minus one

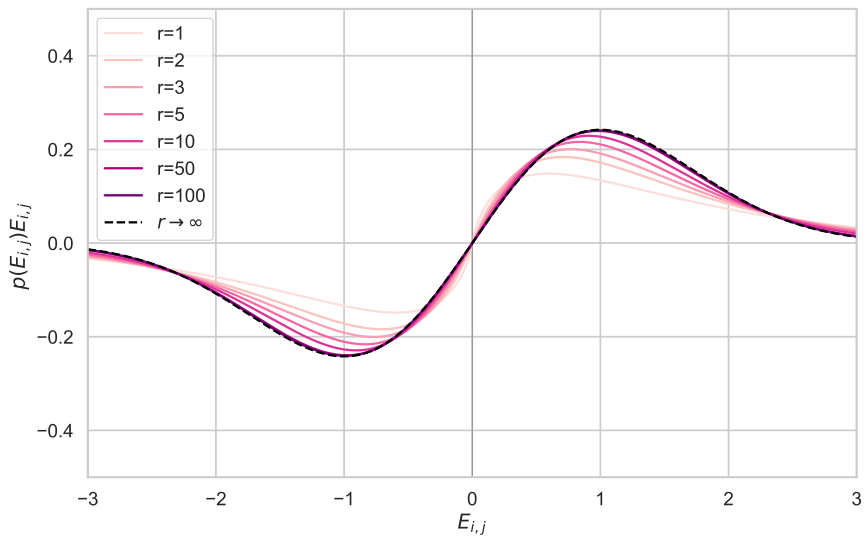

Figure 3: Plot of Marginal Score Multiplied by Density for Increasing r

The convergence rate in Eq. (12) is faster than the typical O(r−21)order r to the minus one half rate dictated by the general parametric central limit theorem. Our analysis shows that this is due to the symmetry in our problem under Assumption 1. To obtain our results, we make an Edgeworth expansion (Bhattacharya & Ranga Rao, 1976) of the distribution P(Er)P of E r, which expands P(Er)P of E r as the limiting Gaussian distribution plus a sum of decaying terms that are controlled by the 3rd order and higher cumulants of P(Er)P of E r. Each ith order cumulant term is multiplied by a factor that decays at rate O(r−2i−2)order r to the power of minus i minus two over two. For symmetric zero-mean distributions, all odd cumulants are zero (for the same reason that all odd moments of a symmetric distribution are zero). Hence, the rate of convergence to the limiting distribution is controlled by the 4th order term, which has rate O(r−1)order r to the minus one.

Although the full distribution P(Er)P of E r has no general closed-form solution, the distribution over marginals P(Ei,j) is more amenable to analysis. We derive the density of the marginal distribution P(Ei,j) for generalised Gaussian distributed ai,j and bi,j in Section D.1. To illustrate the fast convergence rate, we plot the negative density × score function p(Ei,j)Ei,j for the marginal density p(Ei,j) in Fig. 3 using Gaussian distributed ai,j and bi,j (see Theorem 6 for a derivation). The figure shows that p(Ei,j)Ei,j quickly converges to the limiting function 2πEi,jexp(−2Ei,j2)E i j over the square root of two pi, times the exponential of minus E i j squared over two, recovering the Gaussian form from the true Gaussian ES update. Even at r=1r equals one, the function is not a poor approximation. After r=10r equals ten, the function has nearly converged and after r=50r equals fifty, the function is visually indistinguishable from the limit, providing evidence for the hypothesis that the low-rank approximation is accurate even for very low-rank regimes r≪min(m,n)r much less than the minimum of m and n.

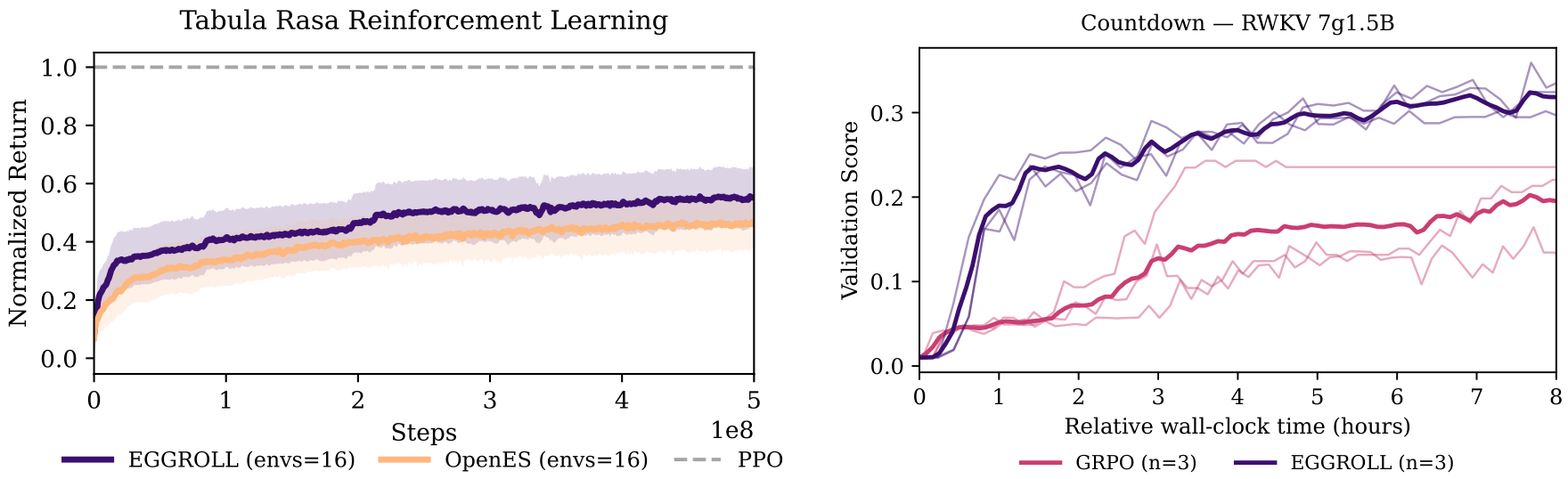

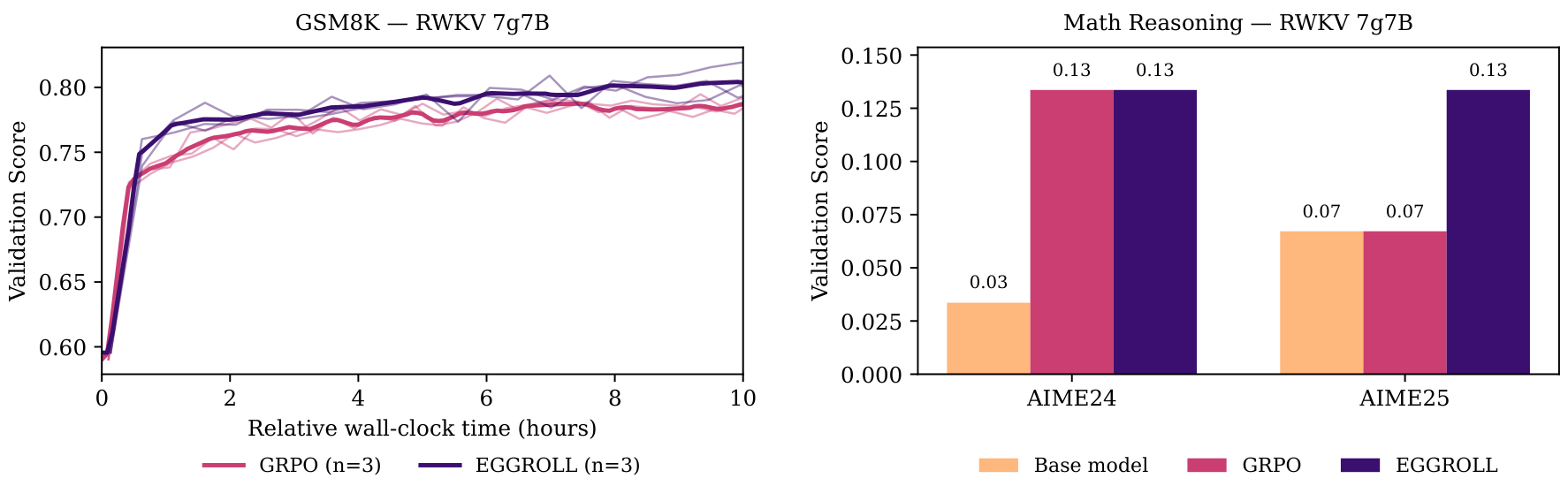

Figure 4: (a) Comparison of reinforcement learning returns normalised by PPO performance across 16 environments for 10 seeds. The shaded region is the standard error of the mean. (b) Validation score of 3 seeds of EGGROLL v.s. 3 seeds of GRPO in countdown task with an RWKV 7g1.5B model on a single GPU. EGGROLL allows 1024 parallel generations per GPU (618 updates) whereas GRPO only 64 (915 updates).

6 Experiments

In the following section we showcase the effectiveness of EGGROLL in a variety of tasks that position it as a strong alternative to back-propagation for the end-to-end training of foundation models.

6.1 Pure Integer Language Model Pretraining

To demonstrate the potential of EGGROLL as a general optimisation method, we apply it to language model pretraining. Since EGGROLL does not rely on gradients, we explicitly design a language model architecture to be efficient and hardware-friendly at inference time. To highlight EGGROLL’s flexibility, we train a nonlinear recurrent neural network (RNN) in pure integer datatypes with no explicit activation functions, relying only on the implicit nonlinearity of clipping in int8 operations. We call the resulting language model EGG, the Evolved Generative GRU, an EGGROLL-friendly architecture with all weights in int8. See Appendix G for more details on the architecture and motivation behind EGG.

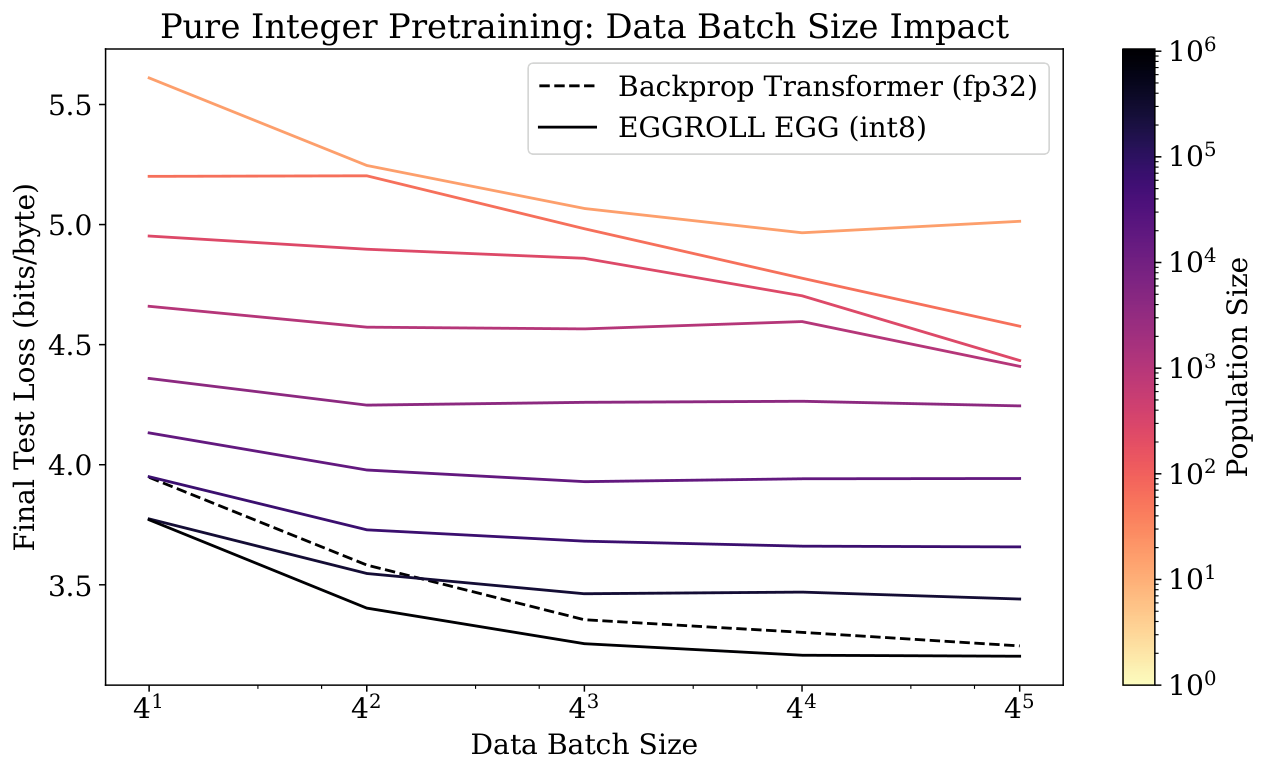

We train an EGG model with 6 layers and hidden dimension 256 (6L-256D) to do character-level prediction on the minipile dataset (Kaddour, 2023). We update parameters after 100 tokens for each population member, applying truncated ES by keeping the hidden state and only resetting at document boundaries. We plot the test loss in Fig. 2b over training steps across a range of population sizes with a fixed data batch size of 16 sequences per step, where the best test loss is 3.40 bits/byte. With a sufficiently large population size, EGG outperforms a dense 6L-256D Transformer trained with backprop SGD using the same data batch size. Note that larger population sizes require more parallel compute for the same amount of data; our largest population size of 220=1048576two to the twentieth power, which is one million forty eight thousand five hundred seventy six requires around 180 times more GPU-hours than the backprop baseline, demonstrating the potential for compute-only scaling in limited data regimes using EGGROLL.

Moreover, our largest population size of 220two to the twentieth is three orders of magnitude larger than the largest experiment done by Salimans et al. (2017)Salimans and colleagues while only requiring a single GPU to train, highlighting EGGROLL’s computational efficiency. We note that large population sizes are critical for pretraining; a population size of 2, analogous to MeZO (Malladi et al., 2023), significantly underperforms larger population sizes despite having access to the same data batch. We conduct more ablations in Appendix I, analysing the tradeoff between population size and data batch size.

6.2 Reinforcement Learning Tasks

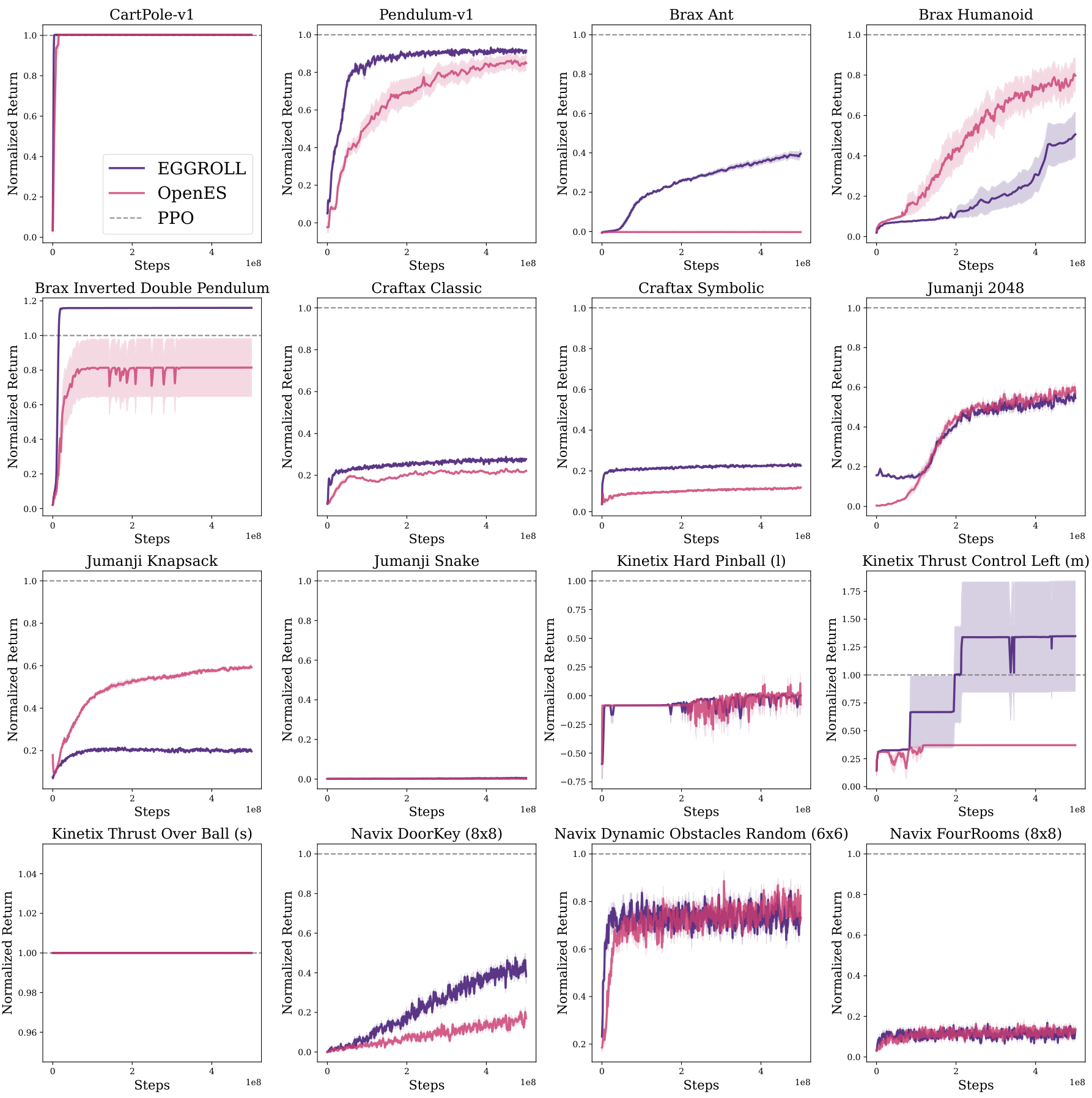

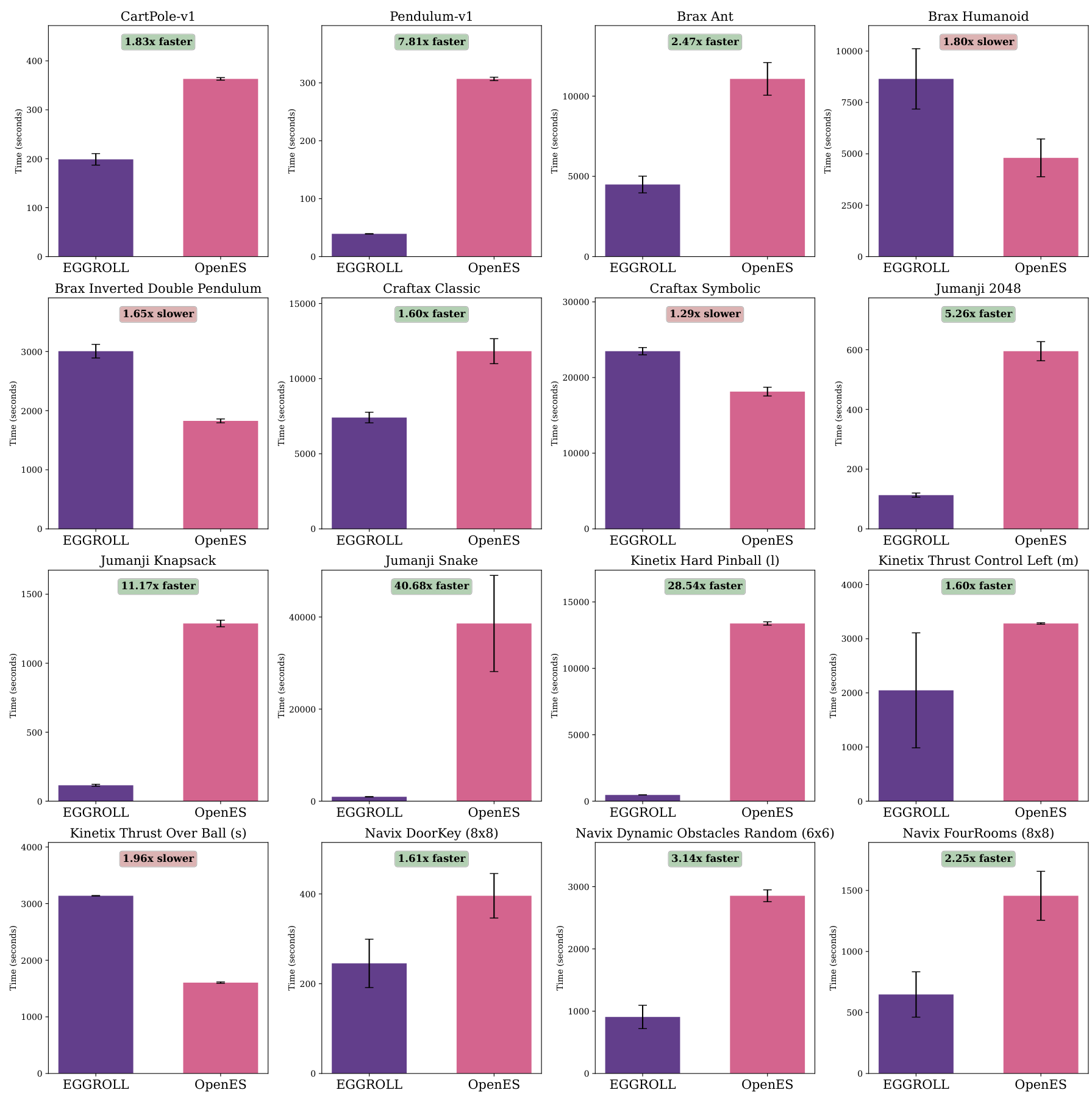

To verify that low-rank perturbations do not change the optimisation behavior of ES in standard control settings, we benchmark EGGROLL against OpenES (Salimans et al., 2017) across 16 tabula rasa environments spanning Navix, Craftax, Brax, Kinetix, and Jumanji. We use a fixed 3-layer MLP policy (256 hidden units) and perform per-environment hyperparameter optimisation for each method before evaluating the selected configuration over 10 random seeds, reporting mean performance (normalised by PPO) and uncertainty. Overall, EGGROLL is competitive with OpenES on 7/16 environments, underperforms on 2/16, and outperforms on 7/16, while often delivering substantial wall-clock improvements due to its batched low-rank structure (full environment

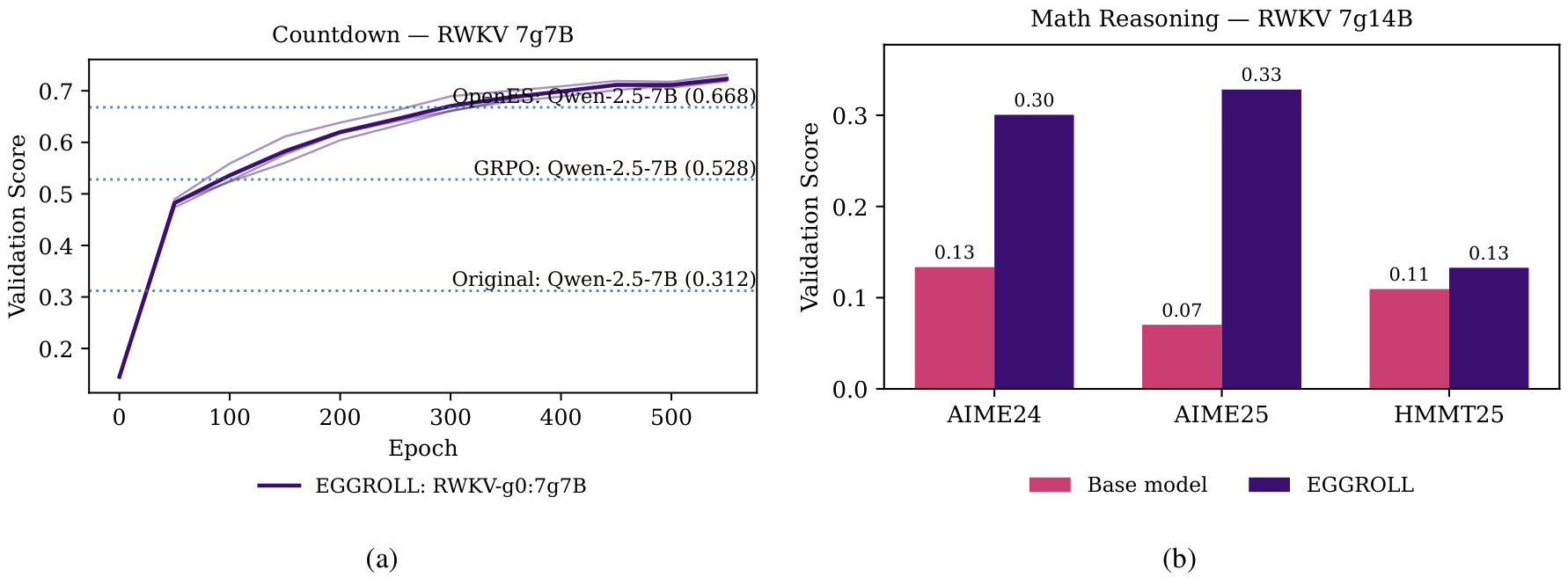

Figure 5: (a) Comparison of the validation score of 3 seeds of EGGROLL v.s. 3 seeds of GRPO in GSM8K task with an RWKV 7g7B model on 8 GPUs. EGGROLL allows 8192 parallel generations (1024 per GPU with 260 updates) whereas GRPO only 256 (32 per GPU with 340 updates). (b) Performance of our finetuned RWKV 7G 7 billion model on hard reasoning tasks using 128 GPUs for 12 hours. The model was trained using the DeepScaleR dataset and the best checkpoint was chosen by evaluating on AIME24.

list, learning curves, timing comparisons, and complete HPO ranges/settings are provided in Appendix N.4. Figure 4a shows the averaged normalised return across the 16 environments with 10 seeds per environment. We additionally report MARL results in Section N.1.

6.3 Foundation Model Fine-tuning

We apply EGGROLL to finetune an RWKV-7 (Peng et al., 2025)Peng and colleagues LLM on two reasoning tasks: countdown (Gandhi et al., 2024)Gandhi and colleagues and GSM8K (Cobbe et al., 2021)Cobbe and colleagues. RWKV is a recurrent model that is better suited to parallelisation than transformers because any memory otherwise spent on the KV cache is used to evaluate population members. Figure 4b shows that EGGROLL fine-tuning on an RWKV-7 1.5B model converges to a higher validation accuracy of 35% (vs. 23%) given the same hardware and wall-clock time in the countdown task. Similarly, Figure 5a shows that EGGROLL outperforms GRPO on GSM8K fine-tuning. Our scoring function draws parallels to the group relative advantage of GRPO. In particular, to score a set of noise directions, E≡{E1,…,En}E, defined as the set E 1 through E n, we first compute their accuracies, {s1,qi,…,sn,qi}s one q i through s n q i, on ∣q∣=mm questions, creating a matrix of scores S∈Rm×nS of dimension m by n. We then compute the normalised score per question, with the main difference that we use the global variance σˉsigma bar, and average over all the questions to compute a score for the noise direction EiE i:

sˉi=m1j=1∑mzi,qj=m1j=1∑mσˉsi,j−μqj.

This scoring function weights all questions within the same batch the same across population members. We use this recipe to train a 14 billion parameter RWKV 7 model on the DeepScaleR dataset and evaluate in more challenging maths reasoning tasks. In this regime, GRPO is infeasible due to the extra memory used by the Adam optimiser Kingma & Ba (2014)Kingma and Ba. Using a thinking budget of 5000 tokens for training and evaluation, our fine-tuned 14B model improves from 13% to 30% accuracy on AIME24, from 7% to 33% accuracy on AIME25 and from 11% to 13% accuracy on HMMT25 after training on 32 GPUs for 12 hours (Figure 13b). On 7B models, we outperform GRPO using 128 GPUs for 24 hours (Figure 5b).

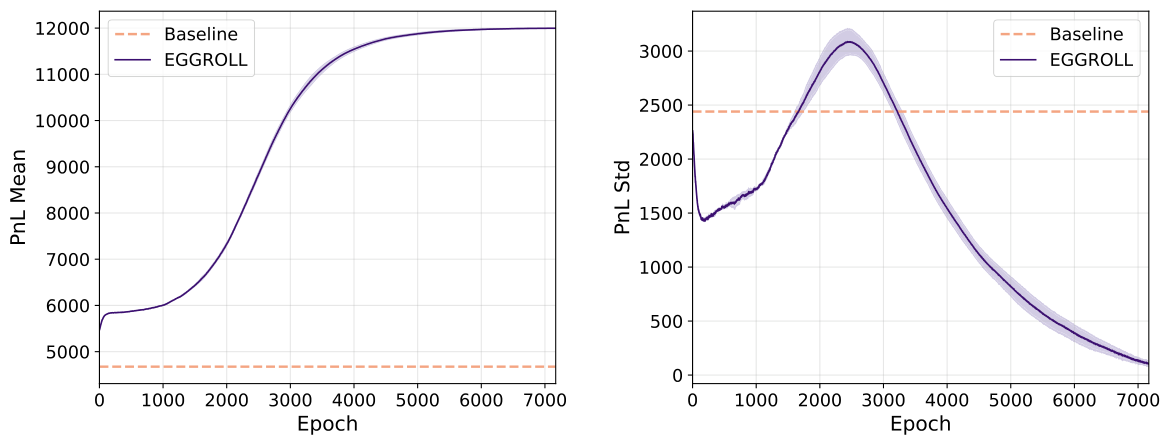

In Section L, we achieve similar performance to GRPO when fine-tuning Qwen Transformer models, and additionally demonstrate that EGGROLL can directly optimise for pass@k, a known limitation of GRPO (Yue et al., 2025)Yue and colleagues. Beyond language models, we also fine-tune a finance world model into an agent for high-frequency trading that directly optimises for PnL; see Section M for more details.

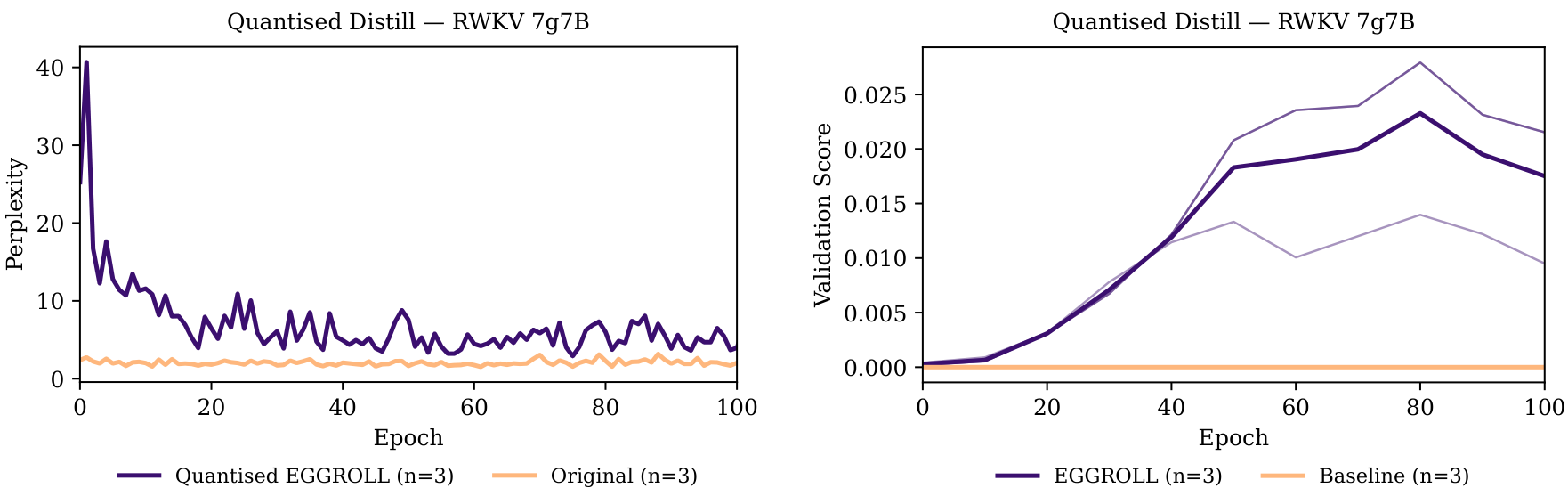

6.4 Fine-tuning Integer Quantised LLMs

We follow the same procedure as Jacob et al. (2017)Jacob and colleagues to quantise the RWKV-7 family of models by dividing by the maximum per-channel value on each weight matrix and mapping into the int8 range of [−127,127]. We then apply EGGROLL with Adam to do model distillation from the original, non-quantised RWKV-7, into the resulting int8 quantised model using examples from GSM8K. See Appendix K for full details about the

Figure 6: (a) Average per token perplexity (during training) of 3 seeds of a quantised (int8) RWKV 7G 7 billion parameter model on distillation from the non quantised model using examples from GSM8K. (b) Validation score on unseen examples of GSM8K of 3 seeds of a quantised RWKV 7G 7 billion parameter model. Initially the model is unable to solve any problems, but progressively it is capable of solving more problems. The baseline here indicates the validation score of a quantised model without any further training.

specifics of quantisation and fine-tuning. The distillation is done by matching the distributions between the quantised and non-quantised models on teacher forced examples (with solutions) from the GSM8K dataset. More specifically, the fitness for a given set of parameters, μimu i, is computed as follows:

fμi(x1:T)=t=1∑TKL(pt∣∣qt(⋅;μi)),

the fitness is calculated as the sum from t equals one to T of the Kullback-Leibler divergence between p sub t and q sub t given mu i

where x1:Tx one through T is a subsequence of tokens taken from the solutions of GSM8K and KL(pt∣∣qt(⋅;μi))the K L divergence is the Kullback-Leibler divergence between the distribution of the non-quantised model, ptp t, and the distribution of the quantised model qtq t over the vocabulary at token tt. Figure 6a shows the average per token perplexity of 3 seeds of a quantised RWKV 7G 7 billion parameter model compared to that of the original non-quantised model over the same sequence, as a baseline. Progressively, the quantised model recovers the capability to solve a subset of the GSM8K dataset (Figure 6b).

7 Conclusion

We introduce EGGROLL, a powerful method for black-box optimisation that scales evolutionary strategies to billion-parameter models and beyond using low-rank search matrices. Our experiments demonstrate that EGGROLL is effective with a rank of 1, giving substantial computational and memory savings for negligible decrease in performance when compared to the full-rank perturbations. Empirically, EGGROLL delivers large speedups over naïve ES in tabula rasa and multi-agent RL, and can power end-to-end training pipelines for foundation models. Our theoretical analysis shows that the EGGROLL update converges towards the Gaussian ES update with increasing rank rr and parameter dimension d=mnd equals m times n, and we provide a rigorous study of general ES at high dimensions, deriving necessary and sufficient conditions for convergence and linearisation.

Looking forward, we can use EGGROLL for other problems beyond the reach of modern first-order gradient-based techniques. In particular, EGGROLL can enable the training of large scale end-to-end neurosymbolic systems (Sarker et al., 2021)by Sarker and colleagues with non-differentiable components. For instance, we can train neural networks that interface with symbolic modules for specific functions, like memory or calculations. We can also optimise end-to-end systems of language models, training them to be aware of inference-time harnesses and interactions with other agents in complex systems.

Acknowledgements

Compute for this project is graciously provided by the Isambard-AI National AI Research Resource, under the projects “FLAIR 2025 Moonshot Projects” and “Robustness via Self-Play RL.” Some experiments also used compute generously given by JASMIN, the UK’s collaborative data analysis environment (https://www.jasmin.ac.uk).

Bidipta Sarkar is supported by the Clarendon Fund Scholarship in partnership with a Department of Engineering Science Studentship for his Oxford DPhil. Mattie Fellows is funded by a generous grant from the UKRI Engineering and Physical Sciences Research Council EP/Y028481/1. Juan Agustin Duque is supported by the St-Pierre-Larochelle Scholarship at the University of Montreal and by Aaron Courville’s CIFAR AI Chair in Representations that Generalize Systematically. Jarek Liesen and Theo Wolf are supported by the EPSRC Centre for Doctoral Training in Autonomous Intelligent Machines & Systems EP/Y035070/1. Jarek Liesen is also supported by Sony Interactive Entertainment Europe Ltd. Uljad Berdica is supported by the EPSRC Centre for Doctoral Training in Autonomous Intelligent Machines & Systems EP/S024050/1 and the Rhodes Scholarship. Lukas Seier is supported by the Intelligent Earth CDT with funding from the UKRI grant number EP/Y030907/1. Alexander D. Goldie is funded by the EPSRC Centre for Doctoral Training in Autonomous Intelligent Machines and Systems EP/S024050/1. Jakob Nicolaus Foerster is partially funded by the UKRI grant EP/Y028481/1 (originally selected for funding by the ERC). Jakob Nicolaus Foerster is also supported by the JPMC Research Award and the Amazon Research Award.

We thank Andreas Kirsch for discovering an emergent log-linear scaling law for EGG loss with respect to int8 OPs in this tweet along with other community members for their comments and recommendations during the first arXiv release of this work.

References

[references omitted]

[references omitted]

Jean-Philippe Bouchaud, Julius Bonart, Jonathan Donier, and Martin Gould. Trades, quotes and prices: financial markets under the microscope. Cambridge University Press, 2018.

James Bradbury, Roy Frostig, Peter Hawkins, Matthew James Johnson, Chris Leary, Dougal Maclaurin, George Necula, Adam Paszke, Jake VanderPlas, Skye Wanderman-Milne, and Qiao Zhang. JAX: composable transformations of Python+NumPy programs, 2018. URL GitHub.

Tom B. Brown, Benjamin Mann, Nick Ryder, Melanie Subbiah, Jared Kaplan, Prafulla Dhariwal, Arvind Neelakantan, Pranav Shyam, Girish Sastry, Amanda Askell, Sandhini Agarwal, Ariel Herbert-Voss, Gretchen Krueger, Tom Henighan, Rewon Child, Aditya Ramesh, Daniel M. Ziegler, Jeffrey Wu, Clemens Winter, Christopher Hesse, Mark Chen, Eric Sigler, Mateusz Litwin, Scott Gray, Benjamin Chess, Jack Clark, Christopher Berner, Sam McCandlish, Alec Radford, Ilya Sutskever, and Dario Amodei. Language models are few-shot learners, 2020. URL arXiv.

Lénaïc Chizat, Edouard Oyallon, and Francis Bach. On lazy training in differentiable programming. In H. Wallach, H. Larochelle, A. Beygelzimer, F. d’Alché-Buc, E. Fox, and R. Garnett (eds.), Advances in Neural Information Processing Systems, volume 32. Curran Associates, Inc., 2019. URL NeurIPS.

Krzysztof M Choromanski, Aldo Pacchiano, Jack Parker-Holder, Yunhao Tang, and Vikas Sindhwani. From complexity to simplicity: Adaptive es-active subspaces for blackbox optimization. In H. Wallach, H. Larochelle, A. Beygelzimer, F. d’Alché-Buc, E. Fox, and R. Garnett (eds.), Advances in Neural Information Processing Systems, volume 32. Curran Associates, Inc., 2019. URL NeurIPS.

Aakanksha Chowdhery, Sharan Narang, Jacob Devlin, Maarten Bosma, Gaurav Mishra, Adam Roberts, Paul Barham, Hyung Won Chung, Charles Sutton, Sebastian Gehrmann, Parker Schuh, Kensen Shi, Sashank Tsvyashchenko, Joshua Maynez, Abhishek Rao, Parker Barnes, Yi Tay, Noam Shazeer, Vinodkumar Prabhakaran, Emily Reif, Nan Du, Ben Hutchinson, Reiner Pope, James Bradbury, Jacob Austin, Michael Isard, Guy Gur-Ari, Pengcheng Yin, Toju Duke, Anselm Levskaya, Sanjay Ghemawat, Sunipa Dev, Henryk Michalewski, Xavier Garcia, Vedant Misra, Kevin Robinson, Liam Fedus, Denny Zhou, Daphne Ippolito, David Luan, Hyeontaek Lim, Barret Zoph, Alexander Spiridonov, Ryan Sepassi, David Dohan, Shivani Agrawal, Mark Omernick, Andrew M. Dai, Thanumalayan Sankaranarayana Pillai, Marie Pellat, Aitor Lewkowycz, Erica Moreira, Rewon Child, Oleksandr Polozov, Katherine Lee, Zongwei Zhou, Xuezhi Wang, Brennan Saeta, Mark Diaz, Orhan Firat, Michele Catasta, Jason Wei, Kathy Meier-Hellstern, Douglas Eck, Jeff Dean, Slav Petrov, and Noah Fiedel. Palm: Scaling language modeling with pathways. J. Mach. Learn. Res., 24(1144), 2023. URL JMLR.

Karl Cobbe, Vineet Kosaraju, Mohammad Bavarian, Mark Chen, Heewoo Jun, Lukasz Kaiser, Matthias Plappert, Jerry Tworek, Jacob Hilton, Reiichiro Nakano, Christopher Hesse, and John Schulman. Training verifiers to solve math word problems. arXiv preprint arXiv:2110.14168, 2021.

A. P. Dawid. Some matrix-variate distribution theory: Notational considerations and a bayesian application. Biometrika, 68(1):265–274, 1981. ISSN 0006-3444.

Nan Du, Yanping Huang, Andrew M. Dai, Simon Tong, Dmitry Lepikhin, Yuanzhong Xu, Maxim Krikun, Yanqi Zhou, Adams Wei Yu, Orhan Firat, Barret Zoph, Liam Fedus, Maarten P. Bosma, Zongwei Zhou, Tao Wang, Emma Wang, Kellie Webster, Marie Pellat, Kevin Robinson, Kathleen Meier-Hellstern, Toju Duke, Lucas Dixon, Kun Zhang, Quoc Le, Yonghui Wu, Zhifeng Chen, and Claire Cui. Glam: Efficient scaling of language models with mixture-of-experts. In Proceedings of the 39th International Conference on Machine Learning, volume 162 of Proceedings of Machine Learning Research, pp. 5547–5569, Jul 2022. URL PMLR.

William Fedus, Barret Zoph, and Noam Shazeer. Switch transformers: scaling to trillion parameter models with simple and efficient sparsity. J. Mach. Learn. Res., 23(1):1–39, January 2022. ISSN 1532-4435. URL JMLR.

In our proofs, we use the integral notation ∫ to denote the integral over the corresponding RdR d space, for example, for a matrix E∈Rm×nE in R m by n, ∫f(E)dE=∫Rm×nf(E)dE and for a vector E∈RmnE in R m n, ∫f(v)dv=∫Rmnf(v)dv. For f:Rd→Rf from R d to R, we use ∇f(x) to denote the derivative of f(⋅) evaluated at x. For a vector v∈Rmnv in R m n, we define the mat operator as:

so mat(vec(M))=M. We will use the fact that the Frobenius norm becomes the ℓ2l two norm in vector space:

∥M∥F=i,j∑mi,j2=k∑vec(M)k2=∥vec(M)∥.(13)

Our proofs make use of Fourier analysis. For a vector-valued function f(v):Rd→R, we define the Fourier transform as:

f~(ω)=F[f](ω):=∫f(v)exp(−iω⊤v)dv,

and the inverse Fourier transform as:

f(v)=F−1[f~](v):=(2π)d1∫f~(ω)exp(iω⊤v)dω,

B ES Matrix Gradient Deviations

Let μM=vec(M)∈Rmnmu M equals vec M in R m n be the vector of mean parameters associated with the matrix M. Let vM∈Rmnv M denote the corresponding search vector associated with μMmu M. As each element of v is generated independently from a standard normal N(0,1), the search vector vM is generated from the standard multivariate norm: vM∼N(0,Imn)v M is sampled from a multivariate normal with mean zero and identity matrix I m n. From Eq. (2), the update for μMmu M is:

We use insights from the Gaussian annulus theorem when investigating the convergence properties of high-dimensional ES: our proof relies on the fact that all probability mass converges to the interior of the ball Bϵ(μ):={x′∣∥x′−μ∥<ϵ}B epsilon of mu, defined as the set of x prime such that the norm of x prime minus mu is less than epsilon where ϵ=2ρepsilon equals rho over two in the limit d→∞d approaches infinity, where ρrho is the radius of the local ball from Assumption 2, meaning we only need to consider the smooth region around μmu in this limit. Our first result proves that the mass outside of the ball for any polynomially bounded function tends to zero at an exponential rate.

Lemma 1 (Polynomial Tail Bounds). Let g(x)g of x be polynomial bounded as:

∥g(μ+σdv)∥≤C∥v∥q(1+∥μ+σdv∥p),

for some finite polynomial of orders p and q and constant C>0. Let Ad:={∥σdv∥≥ϵ} denote the event that a mutation lies outside the a local ball of radius ϵ around μ. Assume σd=o(d−1/2). Then for some constant K>0:

the norm of the expected value of g of mu plus sigma d v, times the indicator function of A d, is big O of d to the power of q over two, times the exponential of negative K times the square of epsilon over sigma d and in particular the right-hand side is o(1) as d→∞.

Proof. We start by bounding the integrand using the polynomial bound. Denote P(Ad):=Ev∼N(0,Id)[1(Ad)]. Then, by Jensen’s inequality in the first line, polynomial boundedness in the second and ∥a+b∥p≤2p−1(∥a∥p+∥b∥p) in the third:

Now, the variable ∥v∥ is χd-distributed. Using the formula for the i-th central moment of ∥v∥ about the origin (Forbes et al., 2011, Chapter 11.3)as described by Forbes and colleagues yields:

Ev∼N(0,Id)[∥v∥i]=22iΓ(21d)Γ(21(d+i)).

Applying the identity Γ(z+b)Γ(z+a)∼za−b(Askey & Roy, 2020-2026, Eq. 5.11.12)from Askey and Roy:

Ev∼N(0,Id)[∥v∥i]∼22i(2d)2i=d2i,(14)

where ∼ denotes asymptotic equivalence. For i=2(p+q), this yields the bound:

We use the Gaussian concentration inequality for the Euclidean norm (Vershynin, 2018, Theorem 3.1.1)from a 2018 paper by Vershynin, which states that for x∼N(0,Id)x distributed as a standard multivariate normal there exists an absolute constant K>0 such that for all t≥0,

Setting t=σdϵ−d, the assumption dσd=o(1)root d times sigma d is little o of one implies for sufficiently large d that dσd≤ϵ and therefore t≥0, so we can apply the concentration bound to obtain:

where we have absorbed the factor of 21 into the constant K. □

Our proof in Lemma 1 reveals the necessity of the condition σdd=o(1) for convergence as we can only apply the Gaussian concentration inequality in Eq. (16) for σdd=o(1); this is a direct consequence of the Gaussian annulus theorem, as for slower rates 1=o(σdd), the Gaussian probability mass will exit any local ball around μ and flood the tail, meaning that the tail probability will grow with increasing d. Having bounded the tail, convergence to linearity follows by proving convergence within the ball, which allows us to exploit the local C1 smoothness of f(x):

Theorem 1 (Convergence to Linearity). Let Assumptions 2, 3 and 4 hold and σd=o(d−21). Then:

∥∇μJ(θ)−∇f(μ)∥=Θ((σdd)α)=o(1),

the norm of the gradient of J minus the gradient of f is big theta of sigma d times root d, to the power of alpha, which is little o of one

almost surely with respect to the distribution over μ.

Proof. We start with the definition of the ES update:

∇μJ(θ)=σd1Ev∼N(0,Id)[v⋅f(μ+σdv)].

Now let ϵ=2ρepsilon equals rho over two where ρrho is the radius of the ball from Assumption 2. Consider the hinge function:

ϕ(x)=⎩⎨⎧1,2−ϵ∥x∥,0,∥x∥≤ϵ,ϵ<∥x∥<2ϵ,∥x∥≥2ϵ,

which interpolates between 1 and 0 in the region ϵ<∥x∥<2ϵ. Our first goal is to use ϕ(x)phi of x to generate a function f~(x)f tilde of x that is absolutely continuous and has integrable derivatives outside of Bρ(μ)B rho of mu to allow us to apply Stein’s lemma (Stein, 1972). We define f~(x)f tilde of x as:

f~(x)=f(x)⋅ϕ(x−μ)

Consider the closed ball Bϵ(μ):={x′∣∥x′−μ∥≤ϵ}. We note that within the ball f(μ+σdv) remains unchanged:

where the gradient fails to exist only on the sets ∥σdv∥∈{ϵ,2ϵ}, which have Lebesgue measure zero. We start by using this function to decompose J(μ)J of mu into a smoothed part and a remainder:

Our goal is to apply Stein’s lemma (Stein, 1972) in its multivariate form (Liu, 1994, Lemma 1). The assumptions of (Liu, 1994, Lemma 1)prior work require that the partial derivatives ∂vif~(μ+σdv) are absolutely continuous almost everywhere and:

Ev∼N(0,Id)[∣∂vif~(μ+σdv)∣]<∞.

These two conditions are satisfied by construction. Indeed, under Assumption 2, f(⋅)f is C1C one continuous on Bρ(μ), hence from Eq. (17), f~(⋅)f tilde coincides with a compactly supported, piecewise C1C one function whose gradient (Eq. (18)) exists almost everywhere. Moreover, under Assumption 3, both f(μ+σdv) and ∇f(μ+σdv) are polynomially bounded, and since ∇f~(μ+σdv) is supported on ∥σdv∥≤2ϵ, it follows that:

Let {μ+σdv∈Bϵ(μ)}={∥σdv∥≤ϵ} denote the event that a mutation lies within the ball Bϵ(μ)B epsilon of mu. We now split the integral into two regions, the first within the ball and the second outside:

Consider the region inside the ball, IlocI local. From Eq. (18), ∇f~(μ+σdv)=∇f(μ+σdv) within this region. Using the local α-Hölder continuity from Assumption 2:

Now, as ∥∇f(μ)∥=O(1) from Assumption 4 and we have established that ∥∇f~(μ+σdv)∥ is polynomial bounded under Assumption 3 when applying Stein’s lemma, it follows that ∥∇f~(μ+σdv)−∇f(μ)∥ is also polynomial bounded, that is there exists some constant C>0 and finite polynomial order p such that:

Again, from Assumption 3, it follows that ∣f(μ+σdv)−f~(μ+σdv)∣ is polynomially bounded, that is there exists some constant C′>0C prime greater than zero and finite polynomial order p′p prime such that:

∣f(μ+σdv)−f~(μ+σdv)∣≤C′(1+∣∣μ+σdv∣∣p).

Applying Lemma 1 with q=1q equals one:

∣∣Δ(μ)∣∣=O(σdd21exp(−K(σdϵ)2)).

Now, as exp(−x)=o(x−1)exponential of minus x is little o of x to the minus one for x→∞x approaching infinity, it follows:

where the final line follows from the fact dσd=o(1)the square root of d times sigma d is little o of one. Assembling our bounds using Ineq. 19 yields our desired result:

We now show that the bound is tight. Consider the function f(x)=2L∑i=1dxi∣xi∣+a⊤xf of x equals L over two times the sum from i equals one to d of x i times the absolute value of x i, plus a transpose x where ∥a∥=O(1)the norm of a is order one. Taking partial derivatives:

∂if(x)=L∣xi∣+ai,(23)

hence:

∥∇f(x)−∇f(y)∥=Li=1∑d(∣xi∣−∣yi∣)2

Applying the reverse triangle inequality ∣∣xi∣−∣yi∣∣≤∣xi−yi∣⟹(∣xi∣−∣yi∣)2≤(xi−yi)2the absolute value of x i minus the absolute value of y i, squared, is less than or equal to x i minus y i, squared:

∥∇f(x)−∇f(y)∥≤Li=1∑d(xi−yi)2=L∥x−y∥.

We have thus shown that f(x)f of x is C1-continuous and its gradient has Lipschitz constant L, i.e. α=1 with Hölder constant L. It is also bounded by a polynomial of order 2. Without loss of generality, we take a deterministic initialisation μ=0mu equals zero to simplify algebra, yielding;

∇f(μ)=a⟹∥∇f(μ)∥=∥a∥=O(1).

f(x)f of x thus satisfies Assumptions 2, 3 and 4.Assumptions two, three and four. Using f(x)f of x as the fitness:

thereby attaining the upper bound rate of σdd. □

C.2 Critical Convergence Rate

To show that our rate is critical, we investigate the space of functions that can be represented by cubic polynomials of the form:

f(x)=a⊤x+21x⊤Bx+61C[x,x,x],(24)

where a∈Rd,B∈Rd×da in R d and B in R d by d is a symmetric matrix and C[x,x,x]=∑i,j,kci,j,kxixjxk denotes a symmetric 3-linear map represented by the 3-tensor C∈Rd×d×dC in R d by d by d.

Since our theory depends on analysing the local stability of a smooth ball for a fitness function, stability over this class is necessary for convergence on more general objectives. We show that once σdsigma d decays slower than the critical rate, divergence already occurs within this subclass, establishing the sharpness of the rate.

Theorem 2 (Exact divergence for cubic objectives).Let f(x)f of x denote the cubic polynomial in Eq. (24). Assume ∥a∥=O(1),∥B∥=O(1),∥C∥=O(1)the norms of a, B, and C are all order one where ∥⋅∥ denotes operator norm for i-tensor T(x1,…,xi): ∥T∥:=sup∥x1∥=⋯=∥xi∥=1∣T(x1,…,xi)∣. Let Assumption 4 hold, then:

where we have used the fact C(v,μ,⋅)=C(μ,v,⋅) by definition of the symmetry of CC. As C(v,μ,⋅)C of v, mu, dot is linear in vv, its expectation under zero-mean N(0,Id)Gaussian noise is zero, hence:

∇μJ(θ)=∇f(μ)+2σd2Ev∼N(0,Id)[C(v,v,⋅)],

proving our first result. Now, it follows that ∥C(v,v,⋅)∥≤∥C∥∥v∥2the norm of C of v, v, dot is less than or equal to the norm of C times the squared norm of v and as ∥C∥=O(1)the norm of C is order one:

Now as vv is unit Gaussian: Ev∼N(0,Id)[∥v∥2]=dthe expectation of the squared norm of v is d, hence:

∥Ev∼N(0,Id)[C(v,v,⋅)]∥=O(d).

We now show that the bound is tight. Consider the function f(x)=u⊤x∥x∥2f of x equals u transpose x times the squared norm of x for u⊤=d1[1,…,1]u transpose equals one over the square root of d times a vector of ones. The factor of d1 ensures that the gradient of the function ∇xf(x)=O(1)the gradient of f is order one. We can write ∥x∥2the squared norm of x as the tensor contraction:

∥x∥2=Id(x,x),

where IdI sub d is the identity matrix and:

u⊤(x)=u(x),

hence we write f(x)f of x as a tensor contraction as:

f(x)=C(x,x,x),

where C:=Sym(u⊗Id)C is defined as the symmetrization of the tensor product of u and the identity matrix. Using this function:

We now study the effect of EGGROLL in high dimensions. We introduce the notation v=vec(E)v equals the vectorization of E to denote the vectorisation of the low-rank matrix perturbation E=r1AB⊤E equals one over the square root of r, times A B transpose and work in vector space. The EGGROLL vector update vv can thus be written as sum of independent variables:

v=i=1∑rr1ui

with:

ui=vec(aibi⊤),

where recall ai and bia sub i and b sub i are the ith column vectors of A and BA and B. We write μ=vec(M)mu equals the vectorization of M. Using Eq. (13), we can convert between results in vector space and matrix space as:

To extend our analysis, we need to ensure that all polynomial moments of P(v)P of v are finite and grow at most polynomially in the dimension d=mnd equals m times n. In particular, such tail bounds are sufficient to dominate polynomial error terms in our analysis. To introduce sub-Gaussian variables, we follow the exposition of Vershynin (2018)Vershynin and results therein. A random variable xi∈Rx sub i in the set of real numbers is sub-Gaussian if there exists some finite constant C>0C greater than zero such that for all t>0t greater than zero:

P(∣xi∣>t)≤2exp(−Ct2),

meaning their their tails decay like Gaussians. This is equivalent to any of the following three properties holding (Vershynin, 2018, 2.6.1): There exist constants C1,C2,C3>0C one, C two, and C three, greater than zero that differ at most by an absolute constant factor such that:

(E[∣xi∣p])p1E[exp(C22xi2)]≤C1p,∀p≥1,≤2,

and if E[xi]=0the expected value of x sub i is zero:

E[exp(λxi)]≤exp(C32λ2),∀λ∈R.

A random vector x∈Rdx in R d is sub-Gaussian if all one-dimensional marginals of xx are sub-Gaussian, i.e. x⊤ux transpose u is sub-Gaussian for all u∈Rdu in R d. The sub-Gaussian norm is defined as:

which returns the smallest universal sub-Gaussian constant for all marginals.

A key property of sub-Gaussian vectors that we use in our proofs is the sub-Gaussian concentration inequality for the Euclidean norm (Vershynin, 2018, Theorem 3.1.1)detailed in Theorem 3.1.1 of Vershynin 2018, which states that for if xx is a sub-Gaussian vector with E[xi2]=1expected value of x i squared equals one and K=∥x∥ψ2K equals the sub-Gaussian norm of x, there exists an absolute constant C>0C greater than zero such that for all t≥0t greater than or equal to zero,

P(∥x∥−m≥t)≤2exp(−K4Ct2).(25)

the probability that the absolute difference between the norm of x and the square root of m is at least t, is less than or equal to two times the exponential of negative C t squared over K to the fourth

We also use a weaker form of control, that replaces the Gaussian-like tail decay with an exponential decay, but all other properties are defined similarly. In this paper, we use the definition that a variable xx is known as sub-exponential if there exists a K>0K greater than zero such that for all t≥0:

P(∣x∣≥t)≤2exp(−Kt).

Our first result derives a bound on the expected value of the norms ∥a∥i and ∥b∥i:

Lemma 2.Let Assumption 6 hold. Let P(a) denote the distribution over columns of A and P(b) denote the distribution over columns of B. Then:

Ea∼P(a)[∥a∥i]=O(m2i),Eb∼P(b)[∥b∥i]=O(n2i).

Proof. It suffices to prove Ea∼P(a)[∥a∥i]=O(m2i) as Eb∼P(b)[∥b∥i]=O(n2i) follows automatically from the same assumptions. We start by using the ‘layer cake’ representation of the expectation Lieb & Loss (2010 - 2010, Theorem 1.13)from Lieb and Loss, Theorem 1.13:

Ea∼P(a)[∥a∥i]=i∫0∞ti−1P(∥a∥>t)dt.

Let tm=Cm for any C>1. We split the integral into two regions:

For the second integral, we wish to bound P(∥a∥>t) for the region t≥tm=Cm. Setting t′=t−m>0, the assumption C>1 implies t′≥0 in this region, hence

P(∥a∥>t)=P(∥a∥−m>t′)≤P(∣∥a∥−m∣>t′).

We bound this using the sub-Gaussian concentration inequality from Eq. (25). Under Assumption 6, a is a sub-Gaussian vector with ∥x∥ψ2≤∞with a finite sub-Gaussian norm, hence there exists an absolute constant C′>0 such that for all t′≥0,

the expected value of the norm of a to the i-th power is big O of m to the i over two

as required. □

Using this result, we now bound the whole vector v=r1∑i=1rvec(aibi⊤)v equals one over the square root of r times the sum from i equals one to r of the vectorization of a i times b i transpose

Lemma 3.Let i≥1. Under Assumption 6:

Ev∼P(v)[∥v∥i]=O((rmn)2i)

the expected value of the norm of v to the i-th power is big O of the quantity r times m times n, all to the i over two

Our proof borrows techniques used to prove linearisation of the ES update in Section C.1 by bounding the tail probability of any polynomial under the low-rank distribution outside of the ball Bρ(μ)B rho of mu. To apply the concentration inequality that would generalise Lemma 1, we show that vv has an exponentially decaying tail:

Lemma 4 (Exponential Tail Bound).Let r<∞r be finite and Assumption 6 hold. Then all elements of vv are sub-exponential and for dσd=o(1)the square root of d times sigma d is little o of one there exists some constant C>0C greater than zero such that:

P(∥σdv∥≥ρ)≤2dexp(−Cdσdρ).

Proof. In matrix form:

E=r1i=1∑raibi⊤.

The elements of EE are thus:

Ej,k=r1i=1∑raijbik.

As aija i j and bikb i k are independent sub-Gaussian random variables with zero mean, it follows from Vershynin (2018, Lemma 2.8.6)Vershynin that their product aijbika i j times b i k is a zero-mean sub-exponential variable with a uniform norm ∥aijbik∥ψ1<∞psi one norm is finite. Finally, a finite sum of sub-exponential variables is sub-exponential (Wainwright, 2019, Eq. (2.18))according to Wainwright with a uniform norm, so all elements of EE and hence v=vec(E)v equals vector E are sub-exponential and zero-mean with a uniform ψ1-norm K<∞psi one norm K is finite.

We now bound P(∥σdv∥≥ρ)=P(∥v∥≥σdρ). For the vector vv, it follows for t≥0:

∥v∥≥t⟹jmax∣vj∣≥dt.

This is easily proven via the contrapositive: if maxj∣vj∣<dt then

As vjv j is a sub-exponential variable with finite uniform sub-exponential norm, by definition (Vershynin, 2018, Proposition 2.8.1)according to work by Vershynin in 2018 there exists a finite KK such that for all jj:

P(∣vj∣≥dt)≤2exp(−dKt).

Applying to Eq. (26) yields:

P(∥v∥≥t)≤2dexp(−dKt).

Now, using t=σdρt equals rho over sigma d and C=K1C equals one over K yields:

P(∥σdv∥≥ρ)≤2dexp(−Cdσdρ).

We now use these results to assemble into our key polynomial tail bound:

Lemma 5 (EGGROLL Polynomial Tail Bounds).Let Assumption 6 hold. Let g(x) be polynomial bounded as:

∥g(x)∥≤C(1+∥x∥p),

for some finite polynomial of order p and constant C>0. Consider the ball Bρ(μ):={x′∣∥x′−μ∥<ρ}. Let {μ+σdv∈/Bρ(μ)}={∥σdv∥≥ρ} denote the event that a mutation lies outside the ball. Assume σd=o(d−1/2). Then for some constant K>0 independent of d: